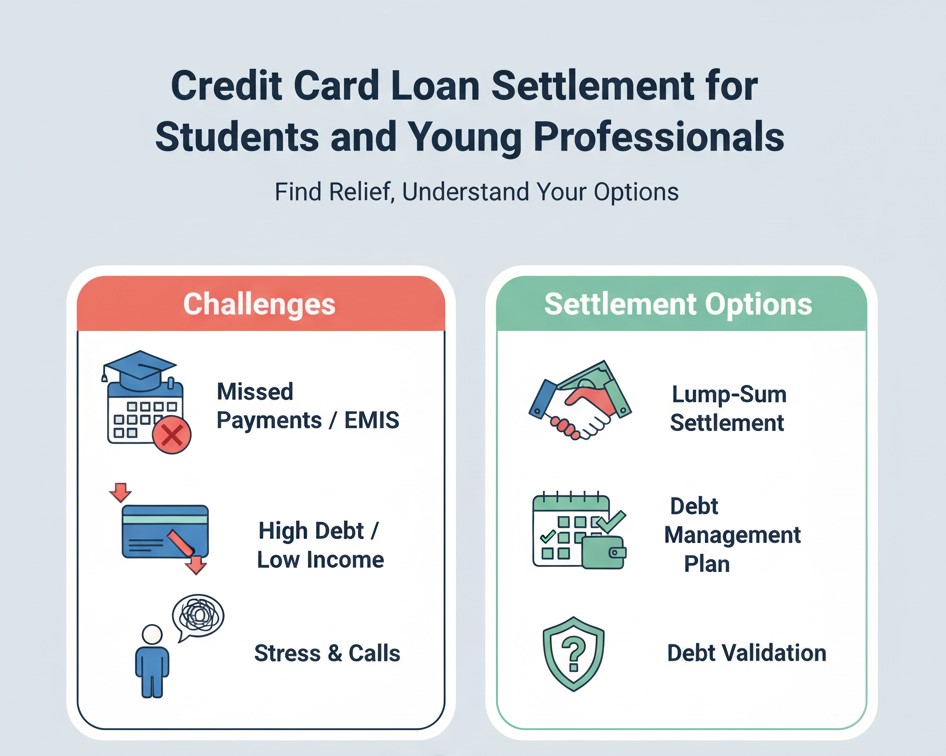

The freedom of a credit card can quickly turn into the heavy weight of the EMI burden. For students and young professionals, who are often managing limited or unstable income, a few large purchases or missed payments can balloon into an overwhelming debt crisis.

If you are a student or a young professional struggling with credit card EMIs, you are not alone. Across the country, many young people are finding themselves caught in this debt trap. The good news is that there is a proven path out: Credit Card Loan Settlement.

Settlement can dramatically reduce your outstanding principal, allowing you to wipe the slate clean and rebuild your financial future.

Why Young Professionals & Students are Prime Candidates for Settlement

Your situation, while stressful, places you in a strong position to negotiate with banks and creditors:

- Lower Earning Potential/Current Hardship: Banks understand that a student or a recent graduate has a significantly limited capacity to repay the full amount. Documenting your current financial hardship—whether it’s a job loss, reduced income, or high student loan burden—gives you strong leverage.

- Unsecured Debt: Credit card debt is unsecured, meaning it is not backed by an asset like a home or car. The bank’s options to recover the full amount are costly (like filing a lawsuit). They would rather settle for a lower, immediate lump sum than spend time and money chasing a full recovery from someone with limited assets.

- High Write-Off Risk: For a bank, receiving 40% of the loan now is far better than waiting years for uncertain payments or facing a total write-off (Non-Performing Asset).

The Path to a Lower Credit Card Loan Settlement

The key to a successful settlement is preparation and negotiation. Here is the clear roadmap:

Step 1: Stop the Bleeding and Assess the Damage

- Halt Credit Usage: Cut up or freeze the credit cards in question. Do not incur any more debt.

- Calculate the True Debt: List every credit card, the current outstanding amount, and the date of your last payment. Include the original principal, fees, and interest.

- Know Your ‘Settlement Budget’: Determine the absolute maximum amount you can realistically gather in the next 30-90 days (from family, savings, etc.). This is your best negotiating chip—a lump-sum payment.

Step 2: The Settlement Negotiation (Aim Low!)

The initial settlement offer from the bank or collector (often 60-70% of the total outstanding) is merely an opening gambit. You must counter it.

- Your Opening Offer: Start your negotiation with an offer of 30% to 40% of the actual principal you borrowed, excluding the crippling fees and penalty interest.

- Leverage Your Situation: Clearly and professionally explain your financial hardship. Stress that your low, lump-sum offer is their best and most immediate chance of recovering funds, far superior to lengthy and expensive legal action.

- The Power of Time: Be patient. Settlement negotiations take time, sometimes weeks or months. The older the account is, the more willing they are to settle for a lower amount.

Step 3: Secure the “Full & Final” Proof

This is the most critical step. Never send a single rupee until you have this document in your hands:

- The Written Offer: Demand a formal Settlement Letter or One-Time Settlement (OTS) Letter on the bank’s letterhead.

- Verify the Terms: This letter must explicitly state that the agreed-upon amount will be accepted as “Full and Final Settlement” of the entire outstanding balance.

- The NOC: It must promise to issue a No-Objection Certificate (NOC) once the settlement payment clears. This NOC is your proof that the debt is fully closed.

Don’t Let the EMI Burden Define Your Career

A credit card settlement will impact your credit score, showing up as “Settled” for several years. However, this is a controlled consequence—it is far better than having a long history of “Missed Payments,” “Default,” or “Charged Off” accounts, which completely cripple your future financial access.

Settlement is a restart button. It cleans up the mess now, allowing you to focus on your career, your savings, and rebuilding a perfect credit profile over the next few years.

Ready to stop the daily EMI anxiety and settle your loan for less?

Let our experts handle the tough conversations and legal documentation to get you the lowest possible settlement.