When financial distress hits, the offer of a One-Time Personal Loan Settlement (OTS) can sound like a miracle cure. It’s the chance to pay a reduced, lump-sum amount and walk away from your debt.

But is this path to debt relief the right move for you? At Settle Loan, we believe in making informed decisions. Here is a balanced look at the pros and cons of a one-time settlement.

What is a One-Time Settlement (OTS)?

A One-Time Settlement is an agreement between you and your lender (bank or NBFC) where you agree to pay a negotiated lump sum—which is less than the total outstanding principal, interest, and penalties—to close your loan account permanently.

The lender agrees to “write off” the remaining balance as a loss.

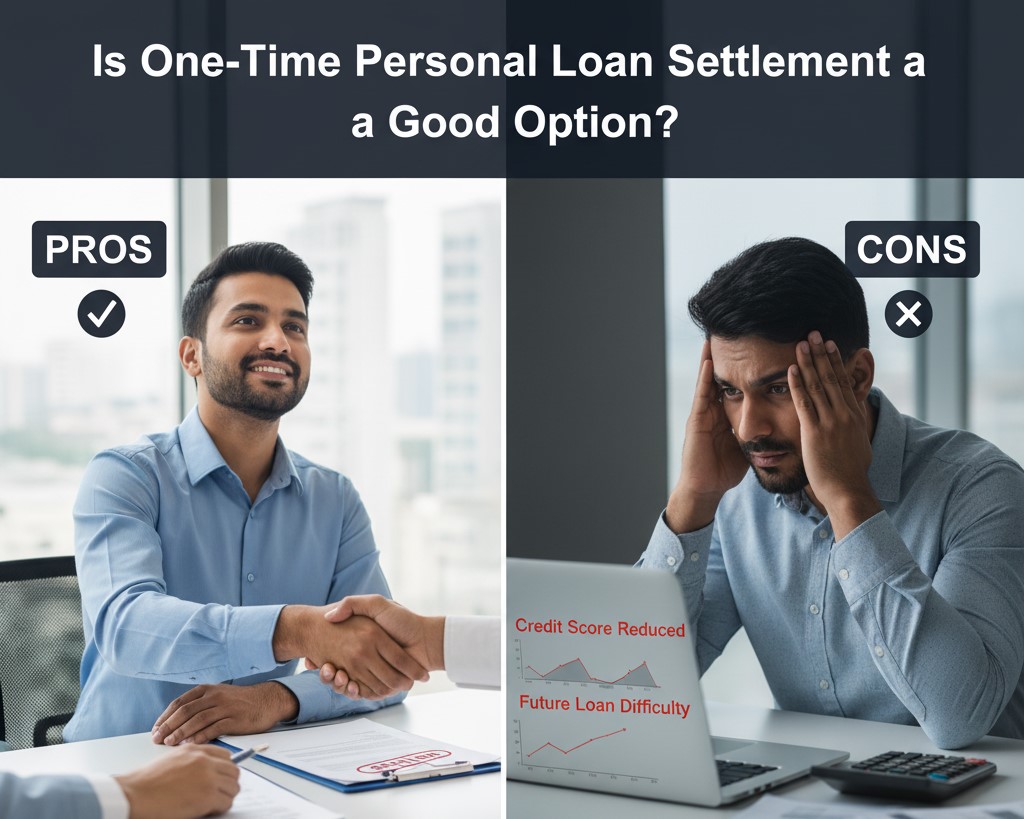

The Pros: Why OTS is a Path to Debt Relief

In situations of genuine financial hardship (like job loss, medical emergency, or business failure), a One-Time Settlement can be an excellent option and a necessary lifeline:

The Cons: The Hidden Cost of Loan Settlement

While the immediate relief is significant, an OTS is not a “loan closure” and comes with a lasting negative impact, primarily on your credit health.

1. The Credit Score Damage (The Biggest Drawback)

- The Status is ‘Settled,’ Not ‘Closed’: Your credit report will show the status of the loan as ‘Settled’ for less than the full amount, not ‘Closed’ or ‘Paid in Full.’ This is a significant red flag for future lenders.

- Major Score Drop: This ‘Settled’ status can cause an immediate and sharp drop in your credit score, often by 75-100 points or more.

- Long-Term Impact: The ‘Settled’ status remains on your credit report for up to 7 years from the date of settlement. This makes it extremely difficult to get a new loan, credit card, or even a home loan for years.

2. Future Borrowing Challenges

Future lenders will view you as a high-risk borrower. Even after the 7-year mark, your settlement history may lead to:

- Rejection of Applications: Being rejected for credit entirely.

- Higher Interest Rates: Being approved only with significantly higher interest rates.

- Lower Credit Limits: Lenders being cautious and offering minimal credit limits.

3. Potential Tax Liability

In some jurisdictions, the portion of the debt that the bank “forgives” (writes off) might be considered as taxable income for you. Always consult a tax advisor to understand the full financial implication of the settlement amount.

Final Verdict: When Should You Settle Loan?

One-Time Settlement should always be considered a last resort.

If you must settle, get expert help to negotiate the best possible terms and, most importantly, secure the legally sound Settlement Letter before paying any money.

Do you need to settle your loan? Don’t go through the process alone.

Our experts can help you negotiate a fair settlement amount and ensure you receive the legal documentation you need to protect your future.