A Loan Settlement (One-Time Settlement or OTS) is often a necessary measure to escape overwhelming debt and stop the fear of defaults. While it offers immediate financial freedom, it leaves a significant, long-lasting scar on your credit profile.

The definitive answer is that a Loan Settlement severely affects your CIBIL Score. It is a major red flag that signals to future lenders that you failed to fulfil your original repayment obligations.

Here is a breakdown of the impact and the strategic steps you must take to repair your creditworthiness after you Settle Loan.

1. The Harsh Reality: Impact of “Settled” Status

The core problem is the status reported by your lender to credit bureaus (like CIBIL, Equifax, etc.):

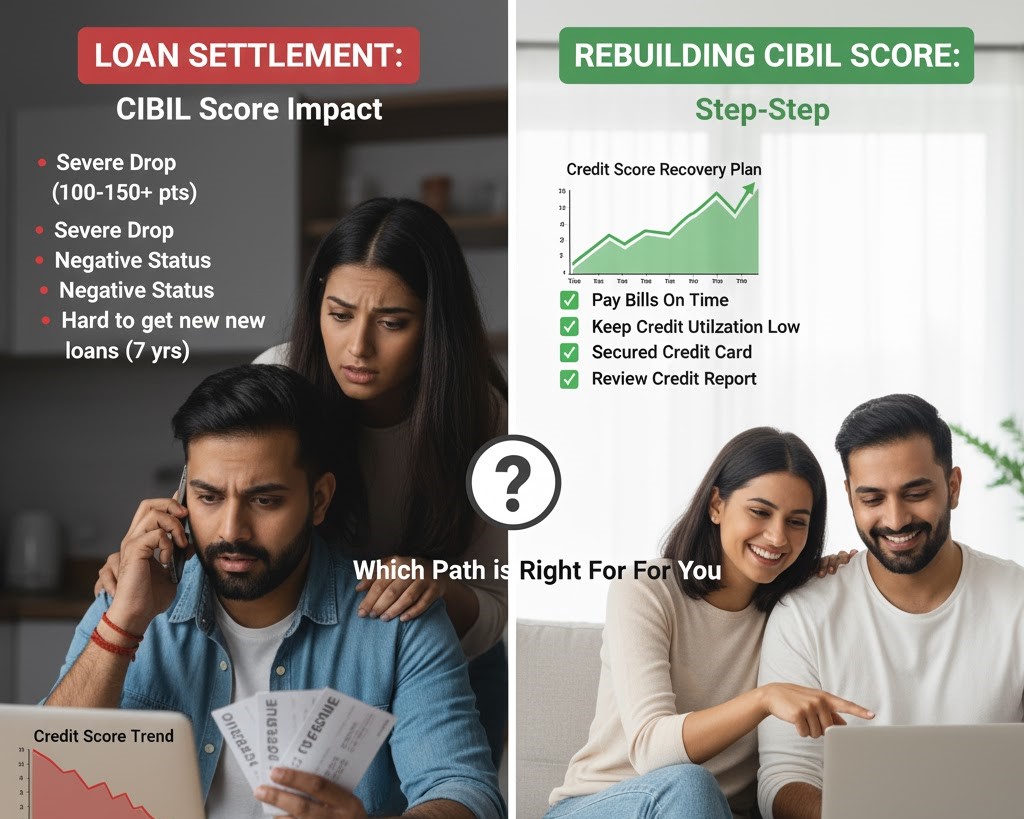

- “Settled” vs. “Closed”: A loan that is “Settled” means you paid less than the full amount contractually due. A loan that is “Closed” means you paid the full amount, principal and interest. This distinction is what costs you credit points.

- Immediate Score Drop: Loan settlement causes a significant, immediate drop in your CIBIL Score, often ranging from 75 to 150 points or more, depending on your prior history.

- Long-Term Visibility: The “Settled” status remains visible on your credit report for up to seven years from the date of settlement. This long-term visibility means that even if your score improves, the negative history is apparent to every potential lender.

- Future Borrowing Difficulties: Lenders view a “Settled” status as a high-risk factor. You will likely face rejection for unsecured loans and credit cards, or be offered credit at significantly higher interest rates and with stricter terms.

2. The Phoenix Strategy: 5 Steps to Repair Your Credit Score

Recovery is a marathon of discipline and patience. Follow these steps to systematically rebuild your credit history.

Step 1: Verify and Correct the Record (The Foundation)

- Obtain the NOC: Ensure you receive the No Objection Certificate (NOC) from the lender immediately after paying the settlement amount.

- Verify Status: Pull your current CIBIL Report. Confirm the settled loan is marked as “Settled” and shows a ₹0 Outstanding Balance.

- Dispute Errors: If the status shows “Written Off” or “Default” without “Settled,” or if any other details are wrong, file a dispute with the credit bureau immediately to correct the error.

Step 2: Pay Everything Else Flawlessly

- Perfect Payment History: This is the single largest factor in your score. For all remaining debts (utilities, rent, existing credit card bills, etc.), make sure payments are made on or before the due date.

- Set Autopay: Utilize automatic payment options to eliminate the chance of accidental late marks.

Step 3: Utilize New Credit Wisely

- Get a Secured Credit Card: If traditional credit is denied, apply for a Secured Credit Card (available against a Fixed Deposit). This allows you to responsibly use and repay credit, building a positive history that is reported to CIBIL.

- Maintain Low Credit Utilization Ratio (CUR): Never use more than 30% of your available credit limit on any card. Ideally, keep it below 10-20%. A high CUR signals financial distress and severely penalizes your score.

Step 4: Avoid “Credit-Hungry” Behaviour

- Limit Hard Inquiries: Do not apply for multiple loans or credit cards in a short period. Each “hard inquiry” temporarily lowers your score and signals desperation to lenders. Be selective and only apply when truly necessary.

Step 5 (Optional but Powerful): Convert “Settled” to “Closed”

- If your financial situation improves, you can approach the lender and offer to pay the remaining waived-off amount from the original loan. If the bank agrees, they can update the status on your CIBIL report from “Settled” to “Closed.” This immediately removes the most significant negative mark and provides a major score boost.

A Loan Settlement closed the door on debt anxiety. Now, by focusing on financial discipline and monitoring your CIBIL Score, you can methodically rebuild your credit profile.

Ready to start your structured credit repair plan?

Contact Us today for expert guidance on navigating the settlement aftermath and rebuilding your CIBIL Score.