The scenario is all too common: you graduate with an Education Loan and the best intentions, only to face a challenging job market. The grace period ends, EMIs begin, and the anxiety of unemployment is compounded by the stress of debt.

If you are currently unemployed after graduation and unable to make payments, you may feel trapped. However, you should know that Education Loan Settlement is absolutely possible with banks and NBFCs in India, provided you approach it strategically and honestly.

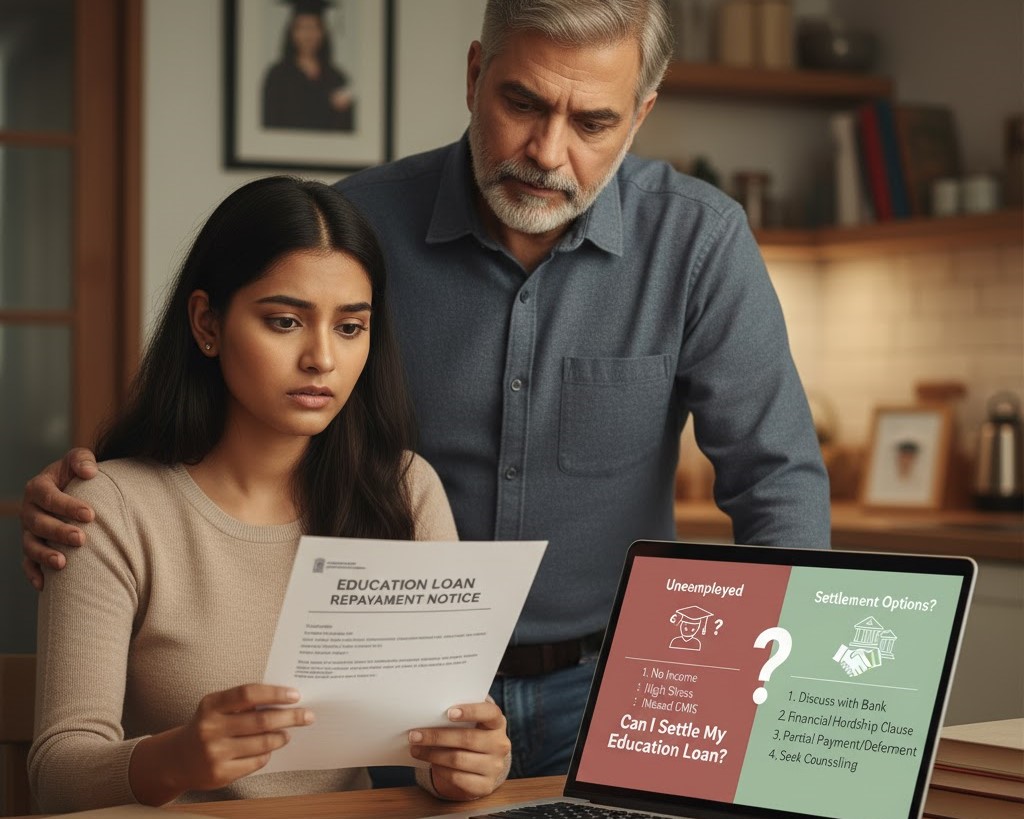

Here is your guide to pursuing a Settle Loan option during unemployment.

1. Why Banks Consider Settlement During Unemployment

Lenders understand that the nature of an education loan is inherently risky, as repayment is contingent on the borrower securing employment. When you are genuinely unemployed, the bank faces a practical reality:

- No Source of Repayment: If you have no income, the bank knows its chances of full recovery are near zero. Waiting years for you to secure a job may result in the loan accruing more unpaid interest and penalties, making the final outstanding amount astronomical and less recoverable.

- Cost of Litigation: Taking legal action against an unemployed graduate with no assets is often costly, time-consuming, and yields poor results.

- Pragmatic Recovery: Banks often prefer to recover a significant lump-sum amount now (even if reduced) through a Loan Settlement rather than holding a Non-Performing Asset (NPA) indefinitely.

2. The Power of Documentation: Proving Hardship

Your success in achieving an Education Loan Settlement while unemployed hinges entirely on your ability to document your financial hardship convincingly.

| Essential Documentation | Why It is Needed |

| Proof of Unemployment | Job Search Evidence: Applications, interview rejections, or proof you are enrolled in skill-building courses. The bank needs to see that you are not wilfully defaulting. |

| Co-Borrower’s Financial Status | Statements showing the parents/co-borrower’s income or financial limitations, proving they cannot service the debt alone. |

| Low-Income Affidavit (if applicable) | A self-declaration detailing zero or minimal income from part-time work or side jobs. |

| Medical/Family Crisis Proof | Any documents related to medical emergencies or family issues that have strained finances. |

3. Strategy: Settlement vs. Restructuring

Before jumping to Loan Settlement (which heavily damages your credit score), you must first propose alternatives.

- Request Restructuring: Formally request the bank to extend your loan tenure, reduce the EMI, or offer a temporary moratorium until you secure employment. This keeps the loan “performing.”

- Propose Settlement: If restructuring is denied, formally submit a written Settle Loan proposal. This proposal should be based on a realistic lump sum that you or your family can raise.

Crucial Point: If you are below the loan threshold for mandatory collateral (often ₹7.5 lakh), the bank’s willingness to settle is usually higher, as they have no asset to seize under the SARFAESI Act.

4. Securing the Final Agreement

When an offer is accepted, proceed with caution:

- Demand a Written Letter: Never pay any amount until you receive a formal, written Settlement Letter from the bank.

- Verify the “Full and Final” Clause: Ensure the letter explicitly states that the lump-sum payment is in “Full and Final Settlement” of the entire loan, and the bank waives all future claims.

While a successful settlement will be marked “Settled” on your credit report for seven years, it provides permanent closure to the debt. Once you find a job, you can focus entirely on rebuilding your career and your Credit Score.

Ready to find a practical solution for your Education Loan? Don’t let debt anxiety overwhelm your job search.