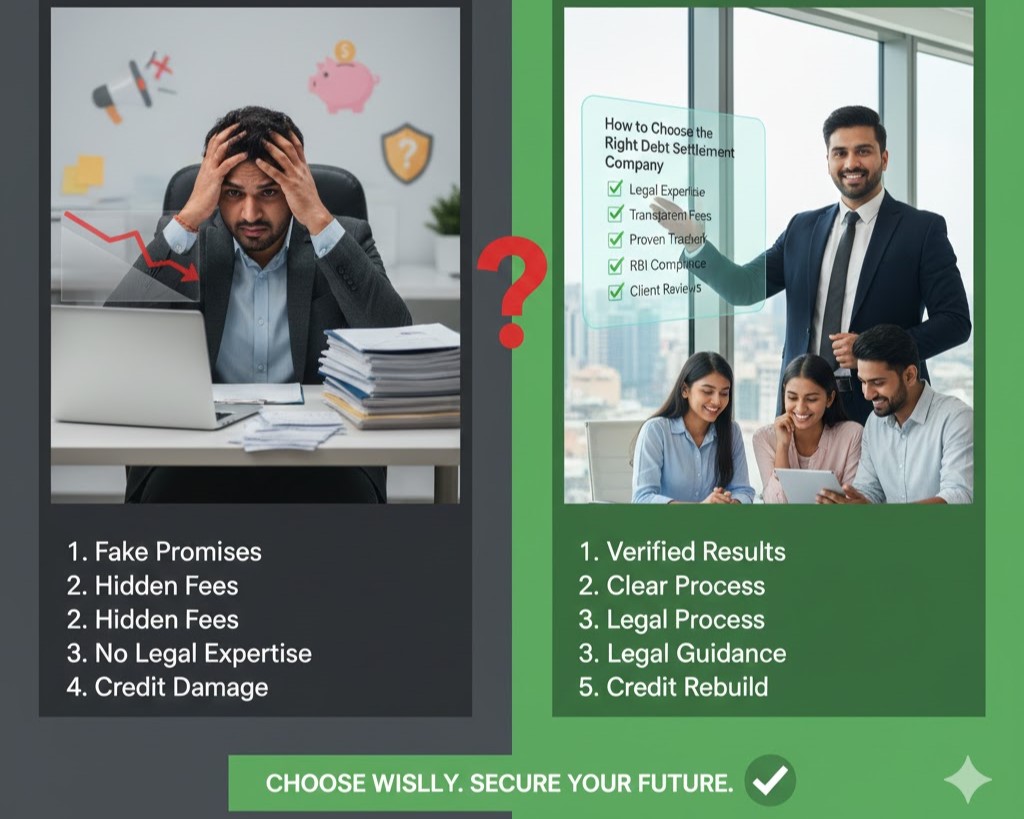

Choosing the right Debt Settlement Company is the most critical decision you will make on your journey to debt closure. A trusted, professional service will secure the maximum possible waiver, protect you from legal pitfalls, and guide your financial planning afterward.

In India, where the debt resolution market is large and often confusing, you need to be highly selective. Here is a definitive guide on how to evaluate and select a truly trusted service for your settlement needs.

1. Verify Credentials and Trusted Service Markers

A professional company operates with transparent legal structures and clear professional standards.

-

Corporate Registration: Ensure the company is a formally registered legal entity (Pvt. Ltd., LLP, etc.). Verify their corporate identity number (CIN/LLPIN) on the Ministry of Corporate Affairs (MCA) website.

-

Expert Panel Credentials: Look beyond generic claims. Does their team include experienced Legal Advisors or advocates specializing in banking laws and debt recovery, or certified Financial Planners? These specialists are essential for both negotiation and documentation.

-

Verifiable History: How long have they been operating? A longer track record suggests stability and experience in dealing with various bank policies. Check for honest client testimonials and case studies (without revealing private financial data).

2. Scrutinize the Fee Structure (Avoid Scams)

The fee structure is the clearest indicator of a trusted service versus a fraudulent operation.

-

Transparency is Key: Demand a written, detailed contract outlining the total service charge, what is included (negotiation, documentation, legal support), and the payment schedule.

-

Success-Based Fees: Reputable debt settlement companies often charge a fee that is either tied to milestones (like final bank approval) or a percentage of the debt saved (the waiver amount). This aligns their incentive with your success.

-

The Golden Rule: NEVER pay the final settlement amount to the company’s account. All final lump sums must be paid directly to the bank via DD or official bank transfer. If a company asks to handle your settlement funds, walk away immediately.

3. 🛡️ Prioritize Legal Protection and Documentation

The primary role of a settlement company is to ensure the debt is closed legally and permanently.

-

No Verbal Promises: A trusted service will insist that all communication with the bank is documented in writing. They should never encourage you to accept a verbal settlement offer from a recovery agent.

-

Documentation Focus: Their process must prioritize securing the two most vital documents:

-

The official Loan Settlement Letter (conditional agreement before payment).

-

The No Dues Certificate (NDC) (final proof of debt closure after payment).

-

-

Credit Reporting Support: A professional partner will also guide you on monitoring your CIBIL report post-settlement and assist you in filing disputes if the status is incorrectly reported (e.g., as “Written-Off”).

4. Focus on Future Financial Planning Guidance

A good settlement company views its role as the start of your financial stability, not just the end of a debt problem.

-

Tax Implications: Do they advise you on the potential tax liability on the waived debt amount and recommend consulting a Chartered Accountant? This shows comprehensive care.

-

Rebuilding Roadmap: They should offer a basic financial planning roadmap for the post-settlement phase, including strategies for rebuilding your credit score and managing your cash flow for future savings.

By meticulously checking a firm’s legal standing, scrutinizing their fees, and verifying their commitment to borrower protection, you can select the right debt settlement company to guide you safely and successfully to debt closure.

Ready to partner with a trusted service?

Contact Us today for a confidential assessment and begin your journey with a transparent and expert debt settlement partner.