Living with the constant weight of unpaid debt is a burden that affects every aspect of life, from mental health to family relationships. In India, where personal loans are easily accessible but come with high interest rates, many borrowers find themselves in a situation where their income is no longer enough to cover their EMIs.

When financial circumstances change due to unforeseen events, a Personal Loan Settlement becomes a vital tool for recovery. This process allows you to close your debt for a fraction of the total amount, providing a clear path to becoming Loan Free. In this guide, we will break down the Loan Settlement Process so you can navigate your way back to financial stability.

What is a Personal Loan Settlement?

A personal loan settlement is an agreement between you and your lender to close the loan account by paying a one-time lump sum that is less than the total outstanding balance. Banks usually consider this option only when a borrower has defaulted for several months and can prove a genuine inability to pay the full amount.

While it is a last resort for the bank, it is a strategic move for a borrower who wants to stop the cycle of mounting interest and penalties. By following the right Loan Settlement Process, you can negotiate a deal that fits your current financial reality.

The Step-by-Step Loan Settlement Process

Navigating a settlement requires a professional approach and a clear understanding of banking procedures. Here is how the journey looks:

1. Assessing Your Financial Situation

Before you begin, you must have a clear picture of your finances. Banks will only agree to a Personal Loan Settlement if they are convinced that you are in a genuine financial crisis. Gather evidence of your hardship, such as medical records, a termination letter from your employer, or proof of a business loss.

2. Communicating with the Lender

Once you have defaulted for a period of three to six months, you should approach the bank’s credit department. It is often more effective to have a professional team like Settle Loan represent you. Experts can articulate your financial situation in a way that the bank understands, making it more likely that they will agree to a settlement rather than continuing with aggressive recovery tactics.

3. The Negotiation Stage

This is the most critical part of the Loan Settlement Process. The bank will initially demand a high amount. You must counter-offer based on the lump sum you can realistically afford. Depending on the age of the debt and the type of lender, settlements can range from 25% to 50% of the total outstanding amount. The goal is to reach a figure that allows you to become Loan Free without further straining your finances.

4. Obtaining the Written Sanction Letter

Never make a payment based on a verbal agreement or a phone call from a recovery agent. You must receive a formal “Settlement Sanction Letter” on the bank’s official letterhead. This letter should clearly state the agreed-upon amount, the payment deadline, and the confirmation that all legal proceedings will be closed once the payment is made.

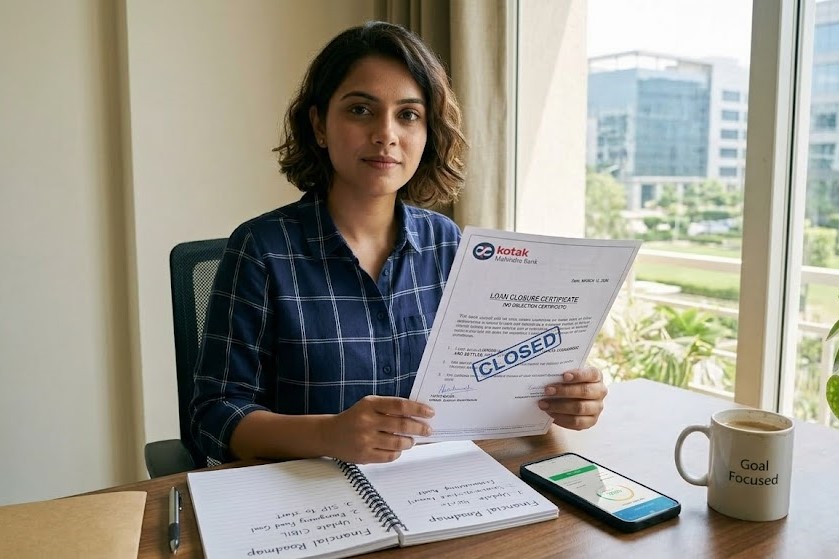

5. Final Payment and Account Closure

After you make the payment as specified in the letter, the bank will process the closure. You should follow up to ensure you receive a “No Dues Certificate.” This document is your legal proof that you no longer owe money to that institution.

Life After Becoming Loan Free

It is important to understand that while a settlement offers immediate relief, it will be reflected on your CIBIL report as “Settled.” This status indicates that the bank took a loss on your account, which may lower your credit score temporarily. However, being “Settled” is far better for your long-term financial health than having an “Active Default” with growing interest.

Once you are Loan Free, you can focus on disciplined financial habits to slowly rebuild your credit score over the next few years.

Why Professional Assistance is Key

Banks are large institutions with experienced legal and recovery teams. For an individual, the Loan Settlement Process can be intimidating and confusing. By partnering with Settle Loan, you gain an advocate who ensures your rights are protected. Professionals can stop the harassment from recovery agents and use their industry expertise to negotiate the best possible terms for your settlement.

Conclusion

Debt does not have to be a permanent state. By understanding the Personal Loan Settlement procedure and taking proactive steps, you can end the stress of unpaid loans. Reclaiming your financial independence is possible with the right guidance and a commitment to moving forward.

If you are ready to start your journey toward becoming Loan Free, visit our experts today to explore your options and find a solution that works for you.