When financial struggles make your car loan unaffordable, a Car Loan Settlement is often the most pragmatic and responsible way to achieve financial closure. It allows you to pay less than the total outstanding amount and close a crippling debt forever.

However, a question often weighs heavily on borrowers’ minds: “How will a Car Loan Settlement affect my CIBIL score and my future credit?”

At Settle Loan, we believe in honest, transparent debt settlement advice. While a settlement is an incredibly effective tool for immediate debt relief, it’s crucial to understand its impact on your CIBIL (or credit score) so you can plan your recovery effectively.

The Unavoidable Truth: The Immediate CIBIL Impact

Any time a lender agrees to accept less than the full amount owed, they report this compromise to the Credit Information Bureau (India) Limited (CIBIL).

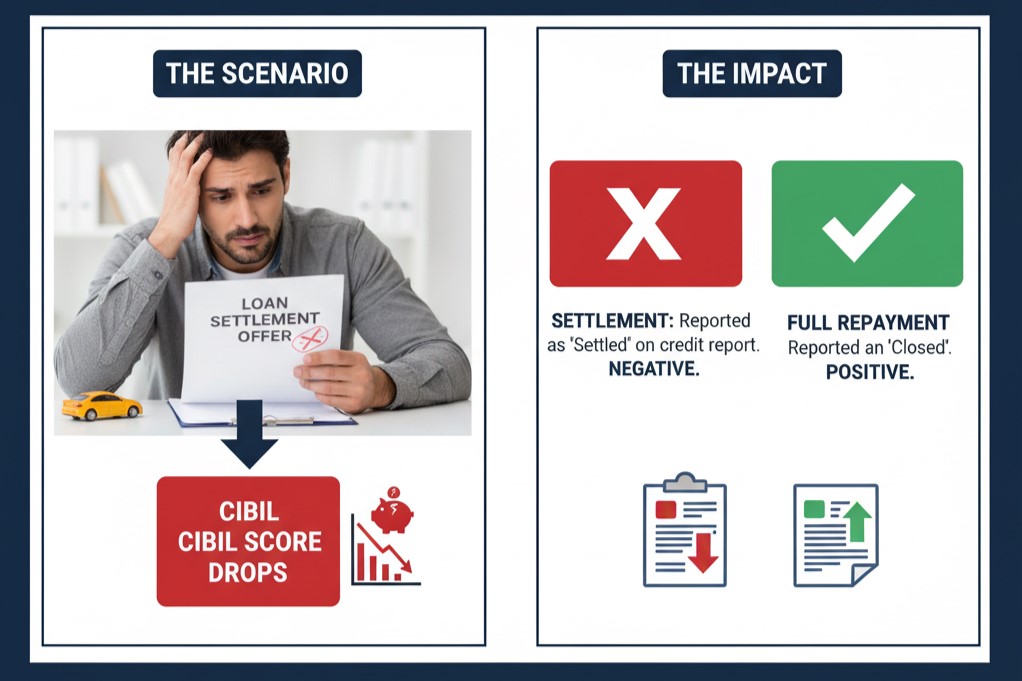

When you achieve a Car Loan Settlement, your report will show the status as “Settled” or “Settled Account.”

- The Immediate Effect: The “Settled” tag is a negative remark. Your credit score (CIBIL) will drop significantly, usually by 100 to 150 points or more, depending on your prior credit history. This impact is unavoidable.

- The Consequence: For the next few years, accessing new loans, credit cards, or lines of credit will be challenging, as lenders view a “Settled” status as a sign of past credit difficulty.

Why “Settled” is Still Infinitely Better Than “Default”

While the initial drop in your CIBIL score is tough, it is vital to compare a Car Loan Settlement to the alternative: Doing Nothing.

The key takeaway: A “Settled” status closes the chapter, allowing you to move forward. An “Unpaid” or “Default” status leaves a financial wound open, bleeding damage into your CIBIL score indefinitely.

Your CIBIL Recovery Strategy with Settle Loan

Our role at Settle Loan doesn’t end when the settlement is approved; we set you up for recovery.

1. Ensure Correct Reporting: The Golden Rule

Upon completing the Car Loan Settlement, we ensure the bank issues a No Due Certificate (NDC) and correctly reports the status to CIBIL as “Settled.” We also verify that the debt amount is zero. An error in reporting (e.g., if the bank mistakenly reports it as “Written Off”) can further complicate recovery, and we are there to fix it.

2. The Path to CIBIL Repair

Once the “Settled” status is confirmed, your recovery can begin. We provide guidance on the steps to repair your credit score, including:

- Taking on new, small, secured credit lines.

- Making all future payments on time (e.g., utility bills, small secured loans).

- Waiting: Over time (typically 2-3 years), the impact of the settlement diminishes as your new, positive payment history grows.

Ready to Close the Debt and Begin Your Recovery?

A Car Loan Settlement is a necessary financial surgery. Yes, there’s a recovery period for your CIBIL score, but it’s the only way to remove the toxic debt that is destroying your financial health right now.

Don’t let the fear of a temporary credit score drop keep you tied to an impossible debt.