When faced with spiraling Credit Card debt, the offer of a Loan Settlement—paying a reduced, lump-sum amount to clear the debt—can feel like a lifeline. But the question is: Is Credit Card Settlement a safe option?

The short answer is: Yes, it is safe, but only in a legal and technical sense. It is a legally binding way to eliminate debt, but it comes with severe, long-term financial consequences that make it a last resort, not a ‘safe’ primary option.

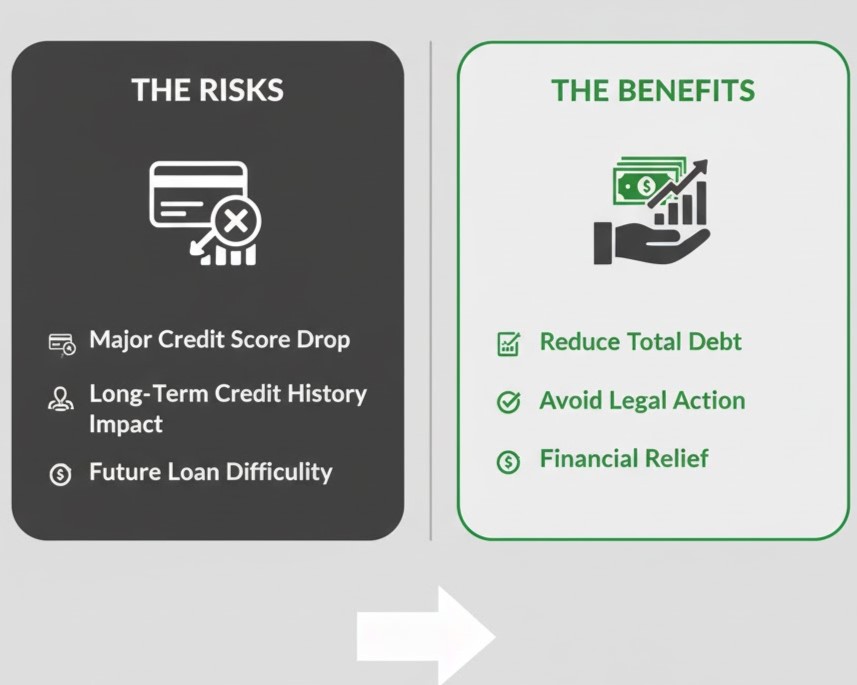

Here is a balanced look at the safety and risks associated with a Credit Card Loan Settlement.

1. The Safety and Finality of a Settle Loan

A properly executed Loan Settlement provides safety in one crucial aspect: legal closure.

- Debt Elimination: Once the negotiated lump sum is paid and you receive the bank’s Settlement Letter, the debt is legally extinguished. The bank cannot pursue you for the remaining waived amount (principal, interest, or penalties).

- Stops Harassment: The legal closure of the account immediately ends the mandate for recovery agents and collection calls related to that specific debt, offering significant psychological relief.

- Avoids Litigation: Settling prevents the bank from filing a civil suit or other legal action against you for the default.

Crucial Safety Precaution: Never pay the settlement amount based on a verbal agreement. Always demand a formal, written Settlement Letter on the bank’s letterhead, explicitly stating the payment is in “Full and Final Settlement.”

2. The Major Risk: Long-Term Credit Damage

The biggest danger of a Credit Card Settlement is the lasting damage it inflicts on your Credit Score and future creditworthiness.

- The “Settled” Mark: Your credit report will display the status of the account as “Settled” instead of “Closed” or “Paid in Full.” The “Settled” status signals to all future lenders that you were unable to repay the full, agreed-upon amount.

- Score Drop: Your Credit Score will take a significant hit (potentially 75 to 150 points or more).

- 7-Year Black Mark: This negative “Settled” status remains visible on your credit report for up to seven years from the date of settlement.

- Future Loan Rejection: For those seven years, securing a new loan, mortgage, or credit card will be extremely difficult. Lenders who do approve you may charge much higher interest rates to offset the perceived risk.

| Account Status | Indication to Lenders | Impact on Credit Score |

| Closed/Paid in Full | Excellent repayment history. | Positive |

| Settled | Inability to repay debt in full. | Highly Negative |

3. Alternatives to Consider First

Because of the severe, long-term consequences on your Credit Score, settlement should only be pursued if all other viable options are exhausted.

- Personal Loan for Consolidation: If you have a decent credit score, take a Personal Loan at a lower interest rate than the credit card’s 30-40% APR. Use this loan to pay off the high-interest credit card debt.

- EMI Conversion: Contact the card issuer and request to convert the outstanding balance into a fixed-tenure, fixed-interest Equated Monthly Installment (EMI) plan. This stops the compounding interest cycle.

- Negotiate Restructuring: If possible, try to negotiate a temporary lower interest rate or extended repayment period instead of a settlement.

The Final Verdict:

A Credit Card Settlement is a secure debt solution that guarantees finality and relief from debt collectors. However, it is not a safe financial decision unless you have absolutely no other means of repayment and are willing to accept years of severely limited borrowing capacity.

Are you overwhelmed by Credit Card debt and need an objective review of your best debt resolution strategy?