When financial hardship hits and you can no longer keep up with monthly payments, both a Personal Loan Settlement and a Credit Card Loan Settlement offer a way out of debt. Both involve negotiating with the lender to pay a lump sum that is less than the total outstanding amount.

However, while the end result—a debt marked as “Settled”—is the same, there are key differences in the negotiation, the debt type, and the amount of leverage you hold. Understanding these distinctions is vital for a successful Settle Loan outcome.

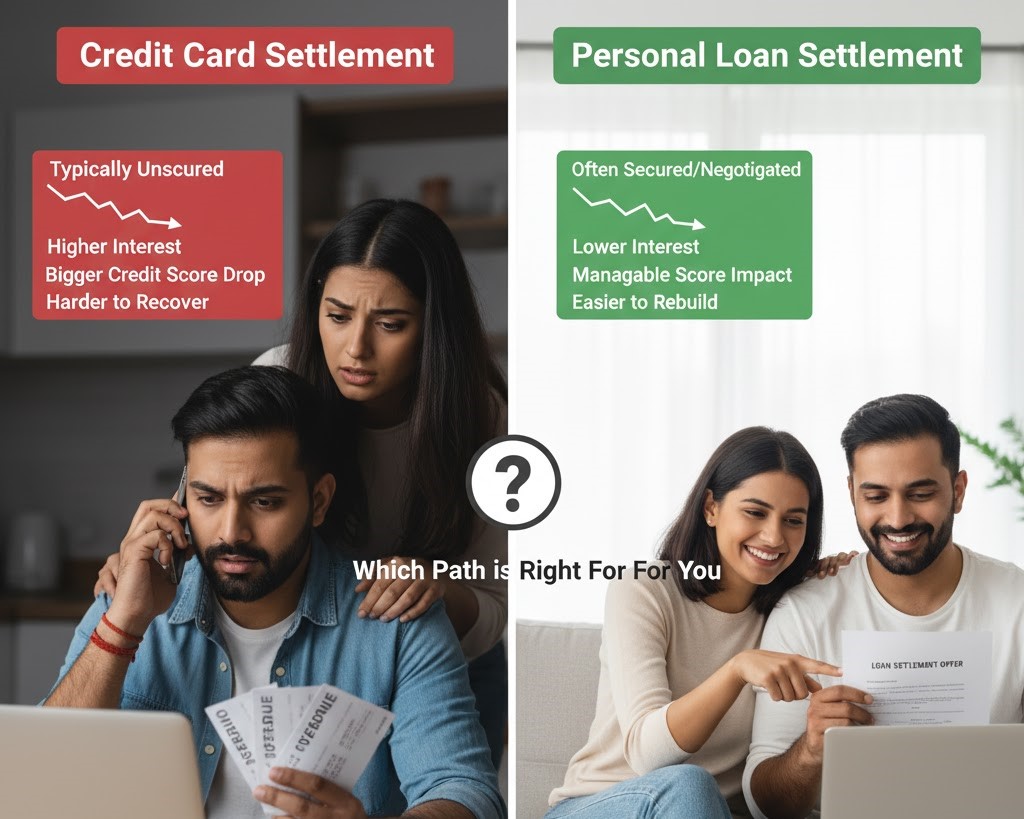

1. The Nature of the Debt: Revolving vs. Term

The fundamental difference lies in how the debt was structured originally.

| Aspect | Personal Loan Settlement | Credit Card Loan Settlement |

| Debt Type | Term Loan: A fixed amount borrowed for a fixed period (tenure) with fixed EMIs. The original principal is clearly defined. | Revolving Credit: A credit limit you can use repeatedly. The outstanding amount fluctuates and includes principal, variable interest, and compounding penalty fees. |

| Interest Rate | Usually lower and fixed or semi-fixed. | Generally much higher (often 35-42% p.a.) and variable, leading to rapid debt escalation. |

| Original Contract | A single, clear loan agreement. | The cardholder agreement is ongoing, and the debt comprises numerous transactions. |

| Escalation | Debt escalates primarily through missed EMI interest and penalties. | Debt escalates very quickly due to high interest, late fees, and compounding charges on the revolving balance. |

2. Negotiation Dynamics and Settlement Amount

While both are negotiations, the amount the lender is willing to forgive can often vary based on the debt type.

- Credit Card Settlement: Due to the extremely high interest and penalty fees accumulated on a credit card, the final outstanding amount is often heavily inflated. Lenders are sometimes more willing to settle for a lower percentage of the total outstanding balance (which includes all the accrued fees) to recover the majority of the original principal amount.

- Personal Loan Settlement: Since the initial interest rate is lower and the debt is structured, the negotiation is often tighter. Lenders typically aim to recover a higher percentage of the principal and accrued interest compared to the inflated final balance on a credit card.

3. Legal and Documentation Triggers

The documentation process for a Settle Loan is slightly different, reflecting the debt’s structure.

- Credit Card Settlement: The focus is on clearing the Statement of Account balance, and the final settlement letter must clearly state the resolution of all associated fees and penalties.

- Personal Loan Settlement: The negotiation centers on the foreclosure/pre-closure statement and the waiver of future interest. The final settlement letter must clearly waive the bank’s right to pursue the remaining future installments.

- Section 138 Risk: For a Personal Loan, failure of an EMI cheque or ECS mandate can trigger a Section 138 (Negotiable Instruments Act) notice, which carries a criminal implication. While this applies to credit card payments as well, the risk for a structured term loan is often clearer.

The Common Consequence: Credit Score Damage

Regardless of whether you settle a personal loan or a credit card debt, the outcome on your credit report is the same:

- The account will be marked as “Settled” (not “Closed”).

- This status indicates you failed to repay the full contractual amount, leading to a significant drop in your credit score.

- The negative mark remains on your credit report for up to seven years, hindering future borrowing.

In both cases, settlement should always be considered a last resort when all other options for full repayment or restructuring have been exhausted.

Ready to explore your best debt resolution strategy for your specific loan type?

Contact Us today for a confidential consultation.