When crushing credit card debt makes your EMIs feel unbearable, a Credit Card Loan Settlement can seem like a beacon of hope. It offers immediate relief by closing the account for a fraction of what you owe. But as a responsible individual planning your financial future, you need to know the full, unvarnished truth: settlement is a double-edged sword that will severely impact your CIBIL Score.

If you are considering settling your loan, read this first.

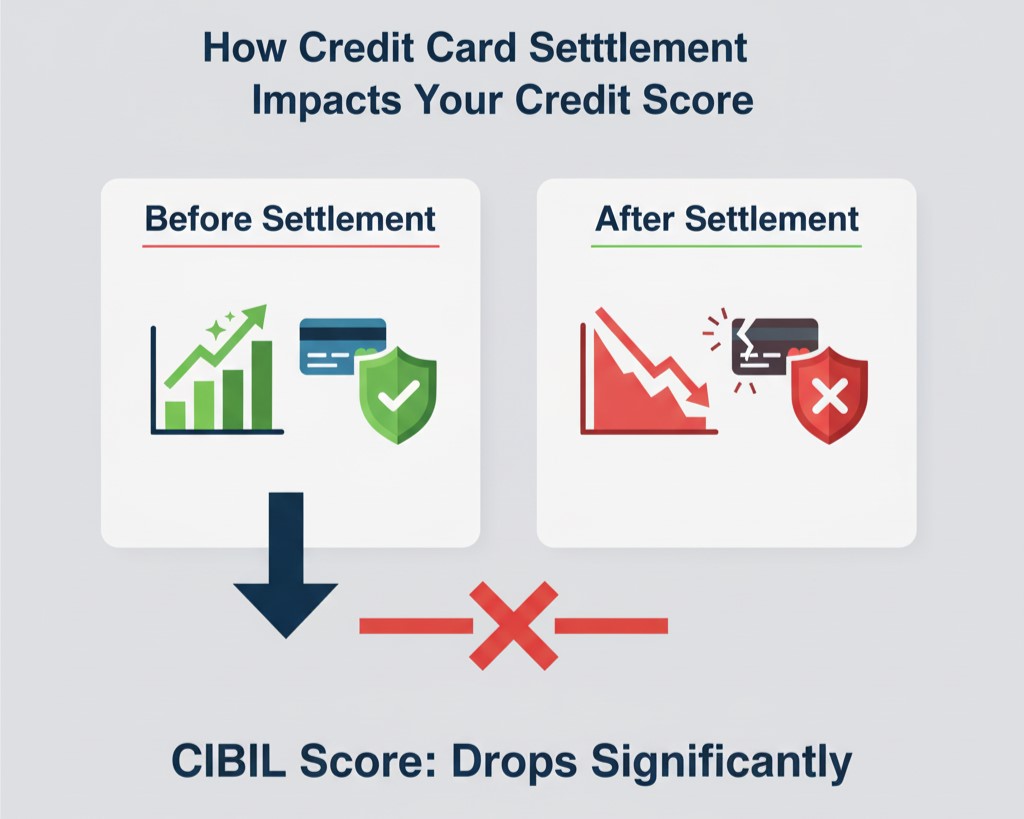

1. The Critical Difference: ‘Settled’ vs. ‘Closed’

The key to understanding the impact lies in the single word the bank reports to the credit bureau (like CIBIL, Experian, etc.):

When you opt for a settlement, the bank reports the account as “Settled.” This status signals to every future lender that you failed to honour the original repayment terms, marking you as a high-risk borrower.

2. The Immediate and Long-Term Damage

A “Settled” mark has a profound and long-lasting effect on your credit profile:

A. The Immediate Drop in CIBIL Score

- Significant Plunge: Expect a sharp, immediate drop of 75 to 150 points or even more, depending on your current score and the amount settled. For someone with an already low score, the impact might be less dramatic, but for a borrower with a decent score, the drop is steep.

- The Pre-Settlement Damage: The negotiation process often involves missing several EMIs, leading to 90-day or 180-day delinquency marks. The score is already plummeting before the settlement is finalised.

B. The Long-Term Visibility (7 Years)

- A Seven-Year Black Mark: The “Settled” status remains on your credit report for a significant period—up to seven years from the date the account was classified as delinquent.

- Future Loan Rejections: During this seven-year window, any application for a major loan (Home Loan, Car Loan, high-value Personal Loan) or a new credit card will be highly scrutinised. Lenders will view the settlement as a major red flag, potentially leading to outright rejection.

- Higher Costs: Even if you are approved for a new line of credit, it will likely be at a much higher interest rate and a lower credit limit, as the lender compensates for the perceived risk.

3. The Hidden Cost: Tax Implications

Beyond the credit score damage, the amount of debt that is forgiven by the lender is typically considered as ‘Income’ under tax laws. This means you may have to pay income tax on the forgiven amount, adding an unexpected financial burden.

4. How to Fix Your Credit Score After a Settlement

If you have already settled a credit card loan, all is not lost, but the path to recovery requires patience and discipline:

- Step 1: Convert ‘Settled’ to ‘Closed’. This is the best way to mitigate the damage. You can still pay the remaining waived-off balance to the bank (if they allow it). Once you pay the full original debt, you can request the lender to report the account status as “Closed” instead of “Settled.” Always get a No Objection Certificate (NOC) in writing and submit a dispute to the credit bureau.

- Step 2: Start Fresh & Pay on Time. The most critical factor in your CIBIL score is your payment history. Ensure every other current and future payment (EMIs, utility bills, etc.) is paid on time, every time.

- Step 3: Maintain Low Credit Utilisation. If you have any other active credit cards, keep the outstanding balance well below 30% of your total credit limit.

- Step 4: Avoid Loan Shopping. Do not apply for unnecessary loans or credit cards. Every inquiry impacts your score.

Don’t Settle Until You Contact Us

Loan settlement is a step of last resort—it’s a financial surgery that saves the patient but leaves a scar. It should only be considered when facing absolute financial distress (e.g., job loss, severe medical emergency) and you have exhausted all other, less damaging options (like a Debt Management Plan or Balance Transfer).

If you are struggling with overwhelming credit card debt, don’t make a decision that impacts your life for the next seven years without professional guidance.

Settle Loan is here to help you explore every available alternative to protect your CIBIL score.

📞 Contact Us Today for a confidential consultation and take control of your debt journey.