When you are struggling with multiple high-interest debts, the options for relief can sound confusingly similar. Two of the most common terms you will hear are Debt Settlement and Debt Consolidation.

While both aim to reduce your financial stress, they are fundamentally different strategies designed for two completely different financial situations. Choosing the wrong one can be a costly mistake.

At Settle Loan, we are experts in navigating the most complex debt resolutions. Here is a clear breakdown to help you determine which path is right for you.

1. Debt Consolidation: The Management Tool

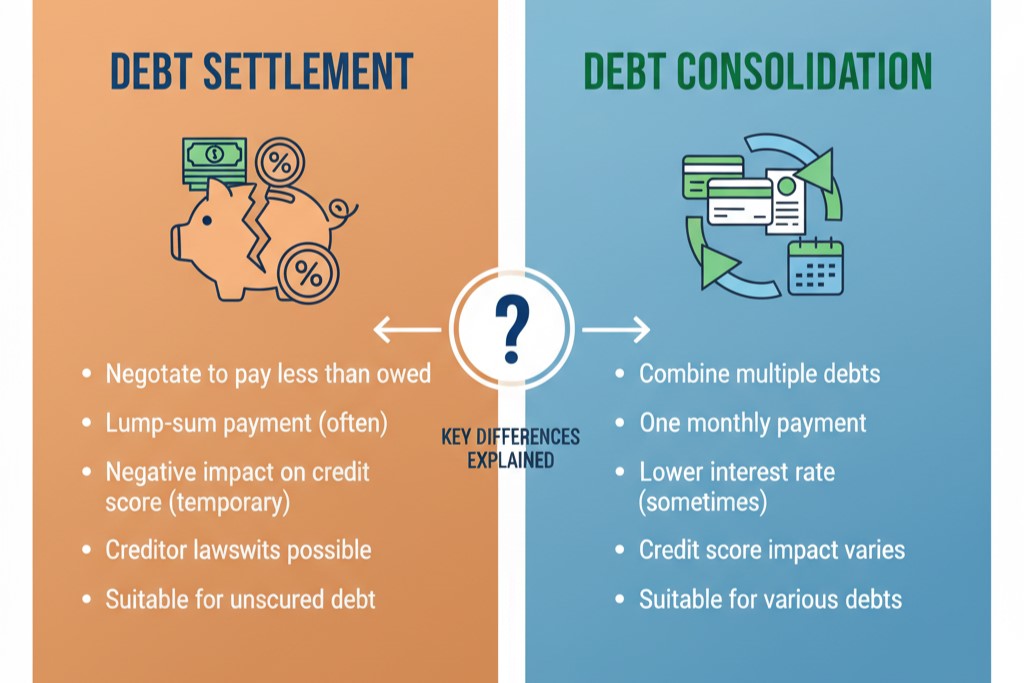

What it is: Debt consolidation is the process of taking out a single, new loan (like a personal loan) to pay off multiple existing debts (like credit cards or other high-interest personal loans).

The Goal: To combine all your EMIs into one simple monthly payment, ideally at a lower overall interest rate. You still pay the full principal amount you owe.

Who Should Choose Debt Consolidation?

Debt consolidation is a strategy for borrowers who are financially stable but overwhelmed by the complexity of multiple payments.

2. Debt Settlement: The Strategic Last Resort

What it is: Debt settlement is a negotiation with your lender to pay a lump-sum amount that is less than the total outstanding principal to completely close the debt account.

The Goal: To reduce the total amount of debt you have to pay to avoid filing for bankruptcy or facing continued legal action. You do not pay the full amount you originally agreed upon.

Who Should Choose Debt Settlement?

Debt settlement is a strategic choice for borrowers who are in severe financial distress and genuinely cannot afford to pay the loan in full.

The Crucial Decision: Which Path to Choose?

Choosing between these two options comes down to a harsh, honest assessment of your financial reality:

Warning: Do NOT choose debt settlement if you can still afford to repay the full amount. The long-term damage to your credit score is not worth the short-term relief.

Why You Need Expert Help for Debt Settlement

If you have determined that debt settlement is your only viable path, do not go it alone.

The process involves complex negotiations, understanding RBI guidelines, and ensuring all legal documents are correct. A lawyer or professional settlement company ensures:

- Best Possible Reduction: They negotiate a lower final settlement amount than you could on your own.

- Legal Protection: They ensure you receive the final, legally binding Settlement Letter and No Dues Certificate to protect you from future claims.

- Correct CIBIL Reporting: They manage the process to minimize errors in how the settlement is reported to credit bureaus.

Don’t let debt define your future. Contact Us Settle Loan today for a free, confidential consultation. We will help you honestly assess your situation and navigate the right path to financial freedom.