When facing significant debt, the question inevitably arises: Is it better to negotiate a Loan Settlement or strive to pay the debt off completely?

This is one of the most critical financial decisions you can make, and the “better” option depends entirely on your current financial stability and your long-term goals. Here is a breakdown of what each option means for your wallet and your credit profile.

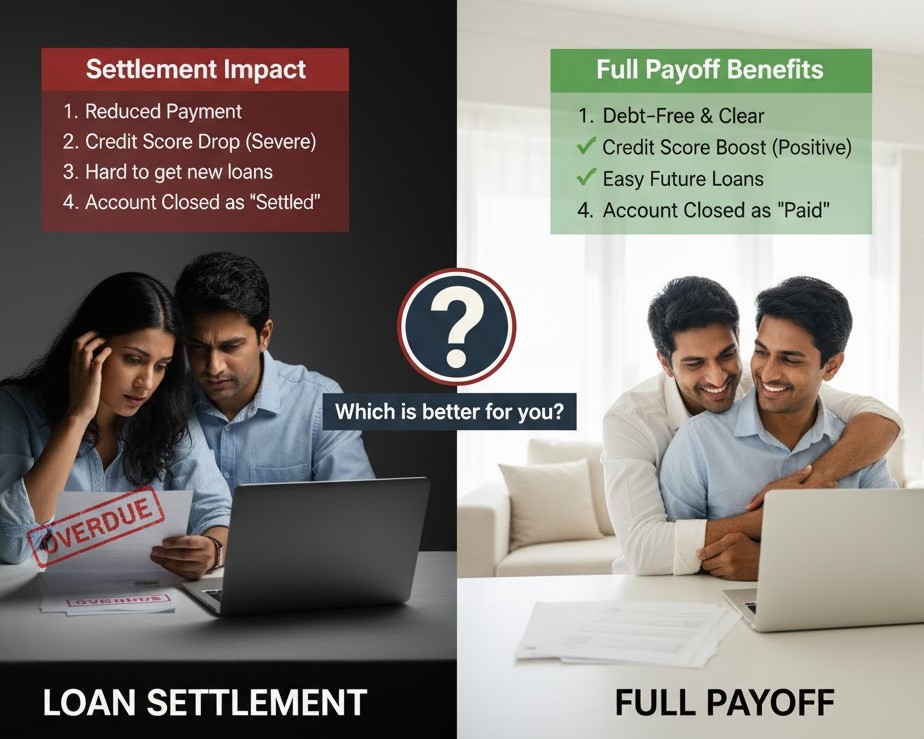

Understanding the Options

| Feature | Paying the Loan Off Completely (Loan Closure) | Loan Settlement |

| Payment Amount | 100% of the principal + interest + charges (as originally agreed). | A negotiated lump-sum amount less than the total outstanding debt. |

| Credit Report Status | “Closed” / “Paid in Full.” This is a positive remark. | “Settled for Less Than Full Balance” or simply “Settled.” This is a negative remark. |

| Credit Score Impact | Positive. Shows you fulfilled your obligation as agreed, boosting your score. | Negative. Causes a significant and immediate drop in your score. |

| Tax Implications | None. | The amount of debt forgiven by the lender may be considered taxable income. |

The Case for Paying the Loan Off Completely

If you have the financial capacity, paying the debt off in full is almost always the superior option for your long-term financial health.

- Credit Health: The account is marked as “Closed” or “Paid in Full” on your credit report. This positive history is the single greatest factor in building a strong credit score, which leads to better interest rates on future mortgages, auto loans, and credit cards.

- Zero Debt: You achieve true freedom from the obligation without the legal or tax complexities that can accompany a settlement.

- Future Borrowing: Lenders see you as a responsible, low-risk borrower, making it easy to secure credit in the future.

The Case for a Loan Settlement

A Loan Settlement should be viewed as a last resort—a necessary lifeline when full repayment is simply not possible due to severe financial hardship (e.g., job loss, long-term illness, or business failure).

When Settling a Loan is the Right Move:

- Imminent Default/Bankruptcy: If you are months behind and facing legal action or bankruptcy, settling the loan, even with the credit damage, is often better than a full charge-off or bankruptcy filing.

- Immediate Relief: It immediately reduces your debt burden and stops the stress of collection calls and late fees.

- Maximum Affordability: If your maximum available lump sum is substantially less than the total owed, a Settle Loan negotiation is your way out.

Important Note on Credit Impact: A “Settled” status on your credit report signifies that you did not pay the debt as originally agreed. This negative mark will remain visible for up to seven years from the date of the first delinquency, making future borrowing expensive and difficult.

Making the Right Choice

- Assess Your Hardship: Are you in genuine, documented financial distress, or are you just looking to save money? If it’s the latter, pay in full. If it’s the former, settlement may be necessary.

- Explore Alternatives: Before choosing a settlement, look into debt consolidation, extended payment plans, or loan restructuring. These options may still allow you to pay the full principal amount, minimizing the credit score damage.

- Calculate the True Cost: Factor in the potential tax liability on the forgiven debt amount when comparing the “savings” of a Settle Loan against the cost of paying in full.

Ultimately, while the immediate relief of a Loan Settlement can be a life raft in a financial storm, paying off your loan completely is the gold standard for long-term credit health.

If you are struggling to make this decision or need expert guidance on how to negotiate a fair settlement without falling prey to poor advice, you can Contact Us for a confidential consultation.