The short answer is Yes, Education Loans can absolutely be settled just like unsecured debts such as Personal Loans and Credit Card dues.

In fact, due to the unique nature of an Education Loan—which is directly tied to the borrower’s future employment—banks often have internal mechanisms and, at times, more compassion when dealing with defaulted education debt compared to other loans.

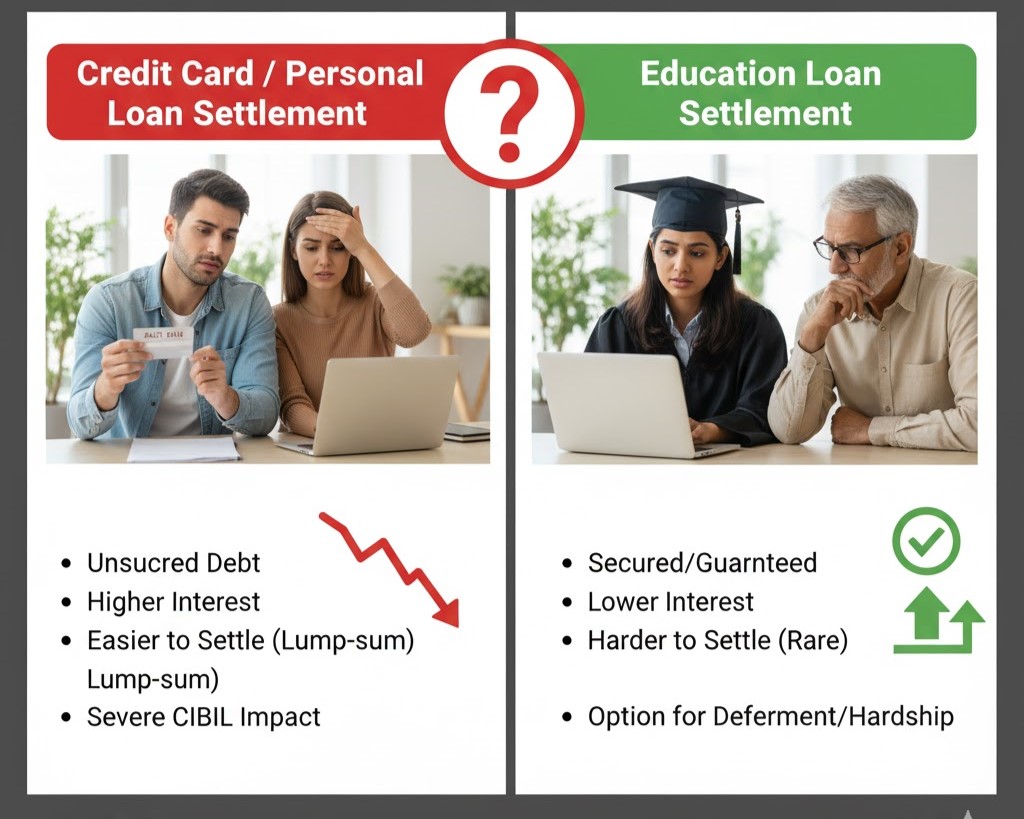

Here is a breakdown of how Education Loan Settlement works, where it differs from a Personal Loan Settlement, and how to pursue your Settle Loan agreement.

1. The Similarities: Why Settlement is Possible

The underlying principle for settling any debt remains the same: the loan has turned into a Non-Performing Asset (NPA), and the bank wants to recover some money rather than zero money.

- NPA Classification: Like a Personal Loan, if your Education Loan EMIs are due for 90 days or more, the account is classified as an NPA, forcing the bank to allocate capital against the loss.

- One-Time Settlement (OTS): The core process is identical. You negotiate to pay a reduced, single lump-sum amount (the OTS amount) to close the entire outstanding balance.

- Credit Score Impact: Just like Personal Loan Settlement, an Education Loan Settlement will be marked as “Settled” on your credit report, severely damaging your Credit Score for up to seven years.

2. The Key Difference: The Nature of the Debt

While the process is similar, the Education Loan context gives you unique leverage that a simple Personal Loan does not.

| Factor | Education Loan Settlement | Personal/Credit Card Loan Settlement |

| Risk Profile | Repayment is dependent on the student securing a job after graduation. This is a known contingency for the bank. | Repayment is based on the borrower’s current documented income and ability to pay. |

| Moratorium Period | Education Loans have a built-in moratorium (grace period). If default occurs immediately after this, the bank is more sensitive to unemployment hardship. | No moratorium period exists; default occurs immediately upon missed payments. |

| Settlement Leverage | Strong leverage if the student is unemployed or underemployed. Banks are often more willing to settle to recover capital before litigation costs rise. | Leverage relies purely on the borrower’s lack of assets and documented extreme financial hardship. |

| Collateral | Loans above ₹7.5 lakhs often require collateral (property, FD). This complicates settlement, as the bank may opt for SARFAESI action over OTS. | Loans are usually unsecured, making settlement the most viable recovery route when the borrower has no assets. |

3. Your Action Plan for an Education Loan Settlement

To successfully settle an Education Loan, you must prove your inability to pay while demonstrating good faith.

- Exhaust Moratorium/Restructuring: Before proposing a settlement, you must first apply for all available moratorium extensions or loan restructuring options (like extending the repayment tenure to reduce the EMI). This proves settlement is a last resort.

- Document Hardship: Compile comprehensive proof of your inability to pay:

- Unemployment letters or a record of job applications/rejections.

- Income proof of parents/co-borrowers showing their financial limitations.

- Any medical or family financial crisis documentation.

- Propose the OTS: Submit a formal, written proposal to the bank’s NPA/Recovery department, detailing your financial situation and the realistic lump-sum amount you can pay.

- Secure Legal Proof: Never pay the settlement amount until you receive a written Settlement Letter on the bank’s letterhead, explicitly stating that the payment is in “Full and Final Settlement” of the entire debt.

An Education Loan Settlement is a powerful option, offering a necessary restart when life doesn’t follow the graduation-to-job plan. Approach it with preparation and strong documentation.