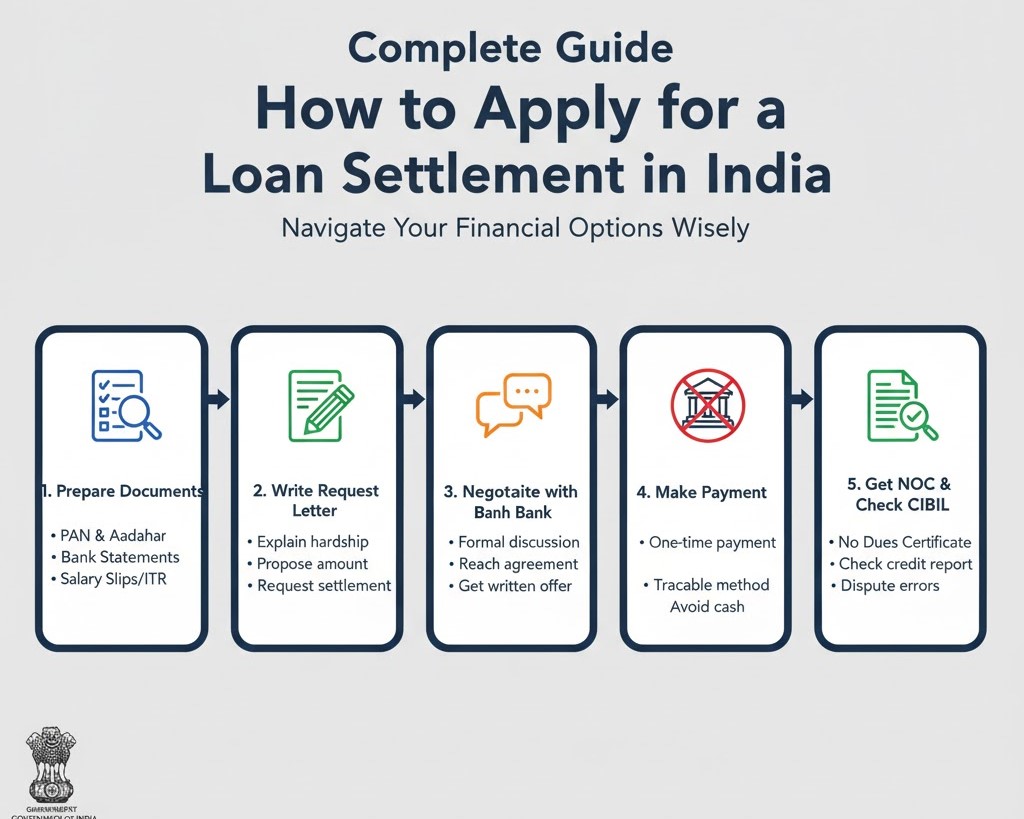

Facing overwhelming debt is stressful, but a Loan Settlement is a definitive, strategic path to financial freedom. This process allows you to negotiate with your lender to pay a reduced, one-time lump sum to close your account, providing immediate debt relief.

The process requires clear communication, meticulous documentation, and smart negotiation. This borrower guide will walk you through the essential steps to successfully apply for and execute a settlement agreement with your bank or NBFC in India.

Step 1: Self-Assessment and Eligibility Check

A Loan Settlement is a last resort, usually considered by lenders only when a borrower is in genuine, verifiable financial distress and the loan has been classified as a Non-Performing Asset (NPA).

-

Financial Distress: You must have a genuine, documented reason for your inability to repay the full loan amount (e.g., job loss, severe medical emergency, business failure).

-

Default Period: Most banks only consider settlement requests for loans that have been in default for at least 6 months. The account should ideally have moved from ‘Overdue’ to ‘Substandard’ or ‘Doubtful’ asset status (NPA).

-

Determine Settlement Capacity: Calculate the maximum lump sum amount you can realistically offer from savings, asset liquidation, or family help. Start with a conservative offer (e.g., 40-50% of the outstanding principal).

Required Documents to Prepare:

-

Proof of Identity & Address (KYC): Aadhaar Card, PAN Card, Passport, etc.

-

Financial Hardship Proof: Job termination letter, medical bills, letter from doctor, or documents proving severe business losses.

-

Income/Financial Proof: Last 6-12 months’ bank statements, latest Income Tax Returns (ITR), and a statement of your current income (if any).

Step 2: Contacting the Lender and Formal Application

Do not wait for the recovery agent; initiate the conversation formally with the bank’s designated department.

-

Approach the Right Channel: Contact the bank’s Grievance Redressal Officer (GRO), the Legal/Collections Department, or the Branch Manager. Avoid negotiating solely with ground-level recovery agents.

-

Submit Written Request: Write a formal application letter requesting a One-Time Settlement (OTS).

-

State the loan account number clearly.

-

Briefly explain the genuine financial hardship.

-

Propose your calculated settlement amount.

-

Attach the hardship documentation.

-

-

Document Everything: Keep copies of the letter, proof of delivery (e.g., registered post receipt), and detailed notes of all conversations, including the name and designation of the person you spoke with.

Step 3: The Negotiation Process

Negotiation is a back-and-forth process. The bank’s first counter-offer will likely be higher than your initial proposal.

-

Be Firm and Realistic: Lenders usually counter-offer in the range of 55-70% of the outstanding principal (excluding waived interest/penalties). Stick close to your maximum capacity, proving that your offer is the best they can realistically recover.

-

Focus on Lump Sum: Lenders prefer a lump-sum payment (One-Time Settlement or OTS) as it closes the account immediately, reducing their risk and administrative burden. If a lump sum is impossible, you may negotiate a short-term, structured repayment plan (e.g., 2-3 months).

-

Negotiate Additional Fees: Ensure that all processing fees, legal charges, and late payment penalties are included in the settlement amount and are not added separately afterwards.

Step 4: Obtain the Formal Settlement Agreement (Crucial Step)

Never make a payment based on a verbal agreement. A formal written document is your only legal protection.

-

Demand a Written Letter: Once a final amount and payment deadline are agreed upon, demand a Loan Settlement Letter on the bank’s official letterhead.

-

Verify Key Terms: The letter must clearly state:

-

The final agreed settlement amount in rupees.

-

The exact deadline for the payment.

-

A statement confirming that the payment will be accepted as full and final satisfaction of the loan, and the remaining balance will be waived.

-

Confirmation that the bank will issue a No Dues Certificate (NDC) after payment.

-

Step 5: Final Payment and Documentation

This final step makes you debt free from that loan.

-

Make the Payment: Pay the agreed lump sum amount strictly before the deadline mentioned in the settlement letter. Keep proof of payment (bank receipt, online transaction confirmation).

-

Collect the NDC: After payment, follow up immediately and ensure you receive the No Dues Certificate (NDC). This legally valid document proves the debt is closed and fully settled.

Step 6: Monitor Your Credit Report

The settlement will be reported negatively, but you must ensure it is reported correctly.

-

Check Status: Verify that your credit report (CIBIL, Experian, etc.) marks the loan as “Settled” and not “Written-Off” or “Defaulted.” A “Settled” status is better than a “Written-Off” status for future credit chances.

-

Dispute Errors: If the status is incorrect, immediately raise a dispute with the credit bureau and the bank, providing the Loan Settlement Letter and NDC as evidence.

While a Loan Settlement negatively impacts your credit score for up to 7 years, it provides immediate financial recovery by eliminating the crushing debt burden, allowing you to begin rebuilding your financial stability.