When you finally secure a One-Time Loan Settlement (OTS) with your lender, the sense of relief is massive. You’ve negotiated a reduced payment, and the promise is simple: pay this lump sum, and the debt is closed. But does this agreement legally remove ALL current and potential legal actions from the bank?

The definitive answer is YES, PROVIDED the settlement agreement is legally watertight, properly executed, and fully complied with.

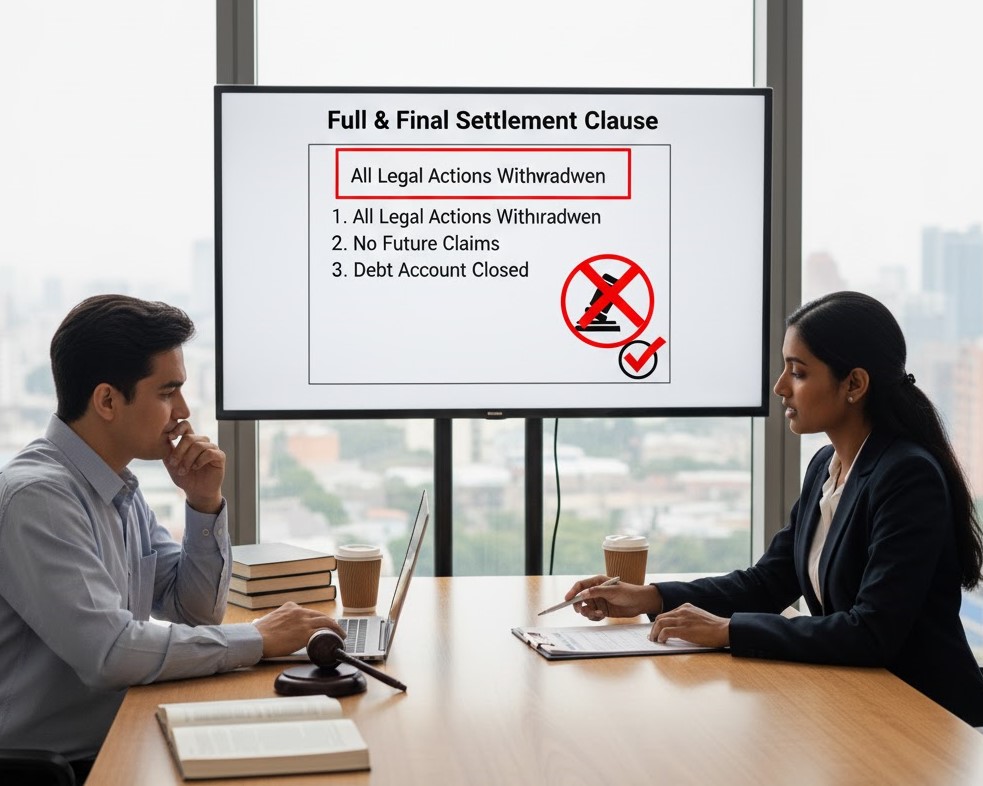

A correctly executed Loan Settlement is a mutual, binding contract that replaces the original loan agreement, legally terminating the debt and extinguishing the bank’s right to pursue recovery in court.

1. The Power of the “Full and Final” Clause

The core function of a One-Time Loan Settlement is to create legal finality. This relies entirely on the language of the final, written agreement.

- Extinguishing the Debt: The settlement letter must explicitly state that the payment of the agreed-upon, reduced sum is in “Full and Final Settlement” of the entire outstanding debt, including the principal, interest, penalties, and all associated recovery or legal costs.

- Waiver of Future Claims: The bank must unequivocally waive its right to pursue the remaining debt amount and any future legal claims related to that specific loan account. This is the clause that legally removes the bank’s ground for litigation.

Crucial Advice: Never make the payment until you have this formal, written Settlement Letter from the bank on their official letterhead, and a legal expert has verified this “Full and Final” language.

2. What Happens to Pending Legal Cases?

If the bank has already filed a case against you (such as a Civil Suit, a case under the Negotiable Instruments Act, or action under the SARFAESI Act for secured loans), the settlement process must include formal legal closure.

- For Cases in Court/Tribunal (DRT): The settlement agreement usually mandates that upon receiving the payment, the bank must file a Consent Decree (or a mutual withdrawal application) with the relevant court or tribunal (like the Debt Recovery Tribunal). This ensures the case is formally closed on the judicial record, not just the bank’s books.

- For SARFAESI Action: If the bank has initiated action to seize collateral, the settlement letter must state that the bank will immediately withdraw all proceedings and return the original property documents and securities upon final payment.

- For Criminal Cases (Sec 138): If a cheque bounce case was filed, the agreement should stipulate that the bank will take the necessary steps to allow the case to be compounded (mutually settled) in court.

3. The Condition for Success: Perfect Compliance

The legal protection of a One-Time Loan Settlement is entirely dependent on the borrower fulfilling their end of the bargain perfectly.

- Timely Payment: You must pay the agreed-upon lump sum amount on or before the exact date stipulated in the settlement letter.

- Lump Sum Preference: Most OTS schemes require a lump-sum payment. Failure to pay on time, or missing a payment in a structured settlement plan (if allowed), can void the entire agreement, reverting the account back to the original full debt amount and allowing the bank to continue legal action.

Warning: A Supreme Court ruling emphasized that a defaulting borrower cannot claim the benefit of an OTS scheme without strictly satisfying all the conditions laid down by the banks, including the requirement of an upfront payment.

A well-executed One-Time Loan Settlement is the absolute legal closure you need. It replaces years of uncertainty and potential litigation with a final, binding contract that eliminates the bank’s right to pursue the debt.

Ready to secure a legally sound Loan Settlement that provides permanent relief from debt and legal threats?