Choosing a Loan Settlement is a powerful, strategic decision that provides immediate debt freedom. However, it is essential to understand the one major trade-off: the negative impact on your CIBIL score and your eligibility for future loans.

While a settlement offers a necessary reset button during a crisis, it temporarily signals to potential lenders that you struggled to meet your original debt obligations. Knowing exactly how the settlement will affect your lending eligibility allows you to plan your financial recovery accurately.

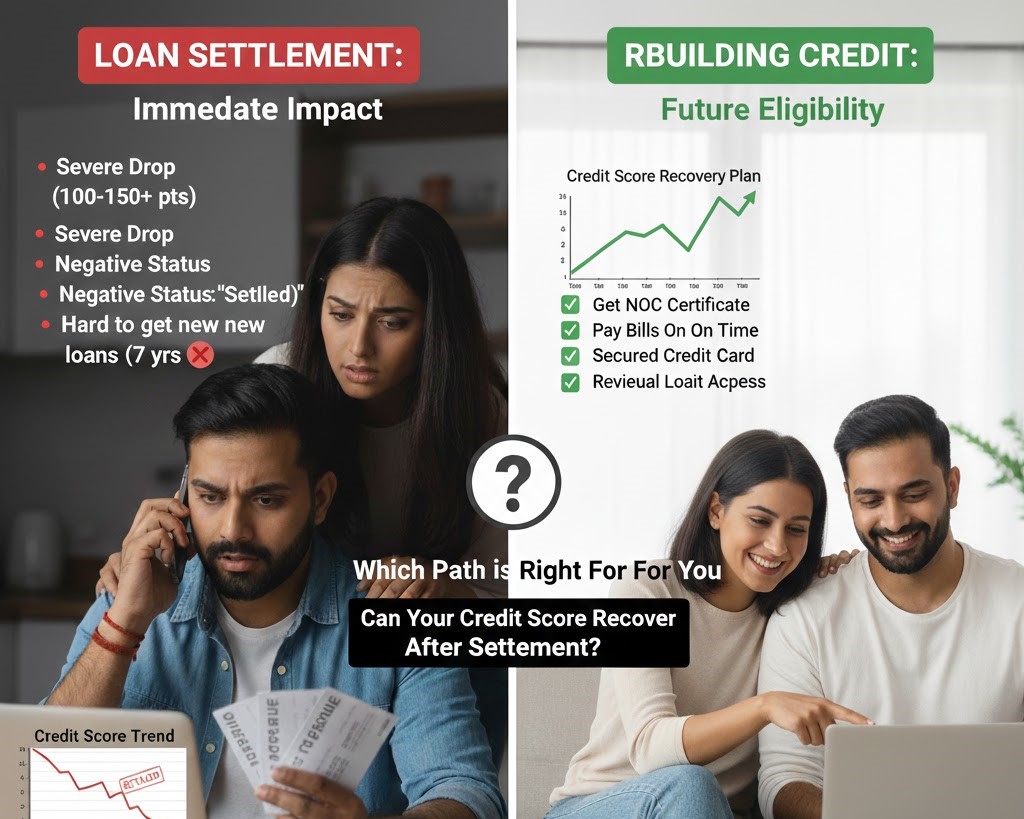

1. The Immediate Hit: Your CIBIL Score Status

Loan Settlement vs. Default/Write-Off

When you settle a loan for less than the full amount, the lender reports the status to all credit bureaus (like CIBIL in India).

-

The Status: The account is marked as “Settled” or “Settled for less than the full amount.”

-

The Impact: This status results in a significant drop in your CIBIL score (typically moving it into the low or poor range, depending on your prior history). This is unavoidable.

-

The Silver Lining: The “Settled” status is generally viewed by credit risk teams as better than an account marked “Default” or “Written-Off.” Settling shows you took proactive responsibility to close the debt rather than ignoring it completely.

2. Impact on Future Loans Eligibility (The Blackout Period)

The “Settled” mark remains on your CIBIL report for up to seven years from the date of settlement. During this period, securing new loans becomes extremely challenging, but not impossible.

| Loan Type | Impact of “Settled” Status | Strategy for Re-Eligibility |

| Secured Loans (Home/Car) | High initial rejection risk. Banks view these as lower risk, but require substantial collateral (60-70% Loan-to-Value). | Wait 2-3 years post-settlement. Maintain perfect payment history on all other debts (like bills/small credit cards) and show high down payment capacity. |

| Unsecured Loans (Credit Cards/Personal) | Near-impossible to obtain from major banks for the first 3-5 years. | Start with secured credit cards (FD-backed) or small loans from specialized financial institutions to rebuild credit history immediately. |

| Small Loans/Micro-Finance | Easier to obtain than large bank loans. | Focus on micro-finance, NBFCs, or specialized lenders who consider current income and recent positive history more than the older settled debt mark. |

3. The Lender’s Perspective: Why They Deny

Future lenders don’t just look at the score; they look at the remarks:

-

Risk Aversion: The “Settled” remark indicates the borrower required special forbearance, signaling higher credit risk.

-

Proof of Rehabilitation: Before lending to you, a bank will require proof of financial recovery—meaning a clean 2-3 year history after the settlement was paid off.

4. How to Accelerate Financial Recovery Post-Settlement

The key to qualifying for future loans is immediately starting a disciplined rebuilding process.

-

Secure the NDC: Ensure you have the No Dues Certificate and that the CIBIL status is correctly marked “Settled.”

-

Perfect Payment History: Pay all current bills, utilities, and any small existing loans on time, every time. Consistency is key.

-

Build New Credit: Obtain an FD-backed secured credit card. Use it sparingly (keep utilization below 10%) and pay the full bill every month. This creates a positive trade line on your CIBIL report.

A Loan Settlement is a necessary short-term tactical move that facilitates long-term financial recovery. Embrace the temporary restriction on future loans as a period to save, strengthen your financial foundations, and prepare for a debt-free future.

Ready to understand your post-settlement credit plan?

Contact Us today for a personalized financial planning strategy to navigate your CIBIL score and accelerate your eligibility for future loans.