When you are facing overwhelming debt and feel like there is no way out, a loan settlement may be a strategic option for you. It’s not a decision to be taken lightly, but it can provide a clear path to becoming debt-free and reclaiming your financial future.

At Settle Loan, we believe in providing you with all the facts so you can make an informed choice and move forward with confidence. Here is a complete guide to understanding loan settlement.

What is Loan Settlement?

A loan settlement (also known as debt settlement) is a negotiated agreement between a borrower and a lender to close a loan account by paying a lump-sum amount that is less than the total outstanding debt.

This is not a regular loan closure. It is a last-resort option for borrowers who are unable to meet their repayment obligations due to severe financial hardship, such as a job loss, a medical emergency, or a sudden reduction in income.

The lender agrees to accept a partial payment because it’s a better alternative than a total default, where they might recover nothing at all.

Key Benefits of a Loan Settlement

While the idea of paying less than what you owe is the most obvious benefit, a loan settlement offers far more than just financial relief.

- Significant Debt Relief: This is the primary advantage. You can significantly reduce your debt burden and get out from under an impossible repayment schedule.

- Avoids Legal Action and Bankruptcy: A settlement provides a legal and formal way to close your debt. This stops the bank from pursuing a total default, which could lead to legal action, asset seizure, or even bankruptcy, all of which have far more severe consequences than a settlement.

- Immediate End to Harassment: Once a settlement is agreed upon and the payment is made, the bank and its collection agents lose their legal right to call you. This can provide immense mental and emotional relief.

- A Fresh Start: By resolving your outstanding debt, you can begin the process of rebuilding your financial health and credit history.

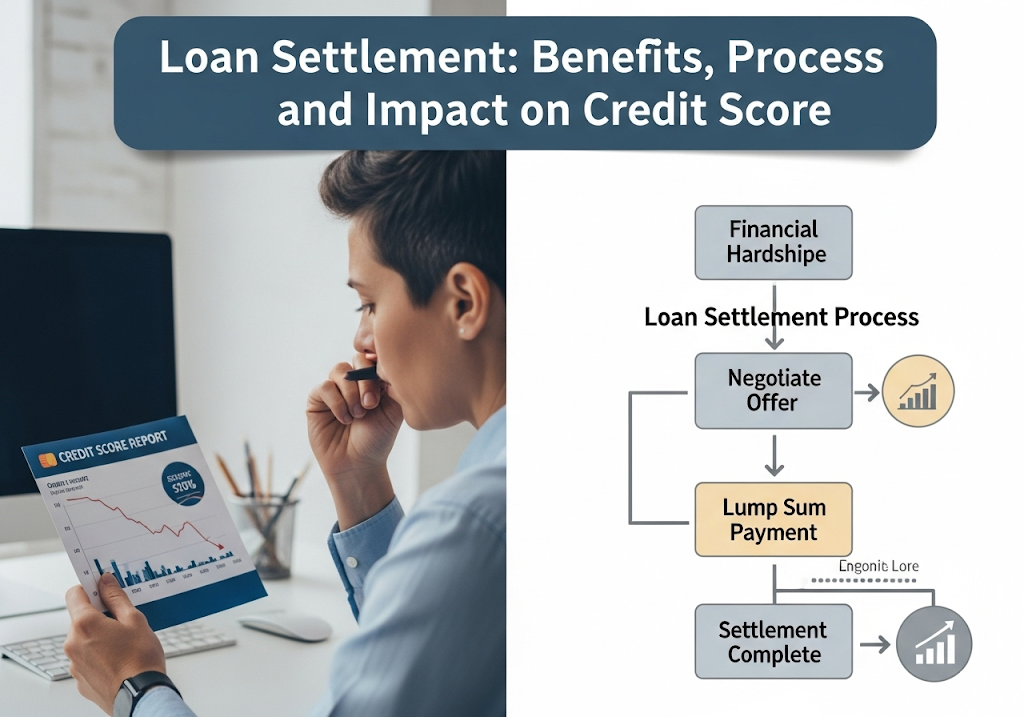

The Process: How to Settle Your Loan

The process of settling a loan requires a clear strategy and careful execution. This is where an expert partner can make all the difference.

- Assess Your Financial Position: Before you approach the bank, you must have a clear picture of your finances. Calculate exactly how much you can realistically afford to pay as a one-time settlement amount.

- Contact Your Lender: You or a legal representative must approach the bank and explain your financial hardship. This is a critical step, as banks are often more willing to negotiate if they see a genuine reason for your inability to pay.

- Negotiate the Settlement Amount: This is the most complex part of the process. You will propose a settlement amount, and the bank may make a counteroffer. The goal is to reach a mutually agreeable figure.

- Get a Formal Agreement in Writing: Do not make a payment based on a verbal agreement. You must receive a formal Settlement Letter from the bank on their letterhead. This document is your legal proof. It must clearly state the agreed-upon amount and confirm that upon payment, the debt will be considered “settled” and the account closed.

- Make the Payment: Once the legal documents are in place, you make the agreed-upon payment by the specified deadline.

- Obtain a No Dues Certificate: After the payment is made, the bank should issue a No Dues Certificate (NDC). This is your final proof that the debt is legally resolved.

- Monitor Your Credit Report: You must check your credit report to ensure the loan status has been correctly updated to “Settled.” If there are any discrepancies, you have the legal documents to get it corrected.

The Impact on Your Credit Score

A loan settlement comes with one significant and unavoidable consequence: it will severely damage your credit score. Your credit report will be marked “Settled,” which indicates to future lenders that you did not repay the full amount. This negative mark will remain for up to 7 years and will make it difficult to get future loans or credit cards.

While this is a serious trade-off, for many, it’s a far better option than a total default or bankruptcy, which have even more damaging long-term effects.

Let Settle Loan Guide Your Path to Freedom

Navigating the complexities of a loan settlement—from the sensitive negotiations to ensuring all legal documents are in place—can be overwhelming.

At Settle Loan, we are experts in this process. We provide:

- Expert Negotiation: We handle all communication and negotiation with the bank to get you the best possible settlement offer.

- Legal Protection: We ensure you have all the correct legal documents to protect you from future claims.

- A Roadmap to Recovery: We don’t just settle your loan; we provide a clear plan for your financial recovery, including tips on how to rebuild your credit score.

Don’t let unmanageable debt define your future. Contact us Settle Loan today for a free consultation and let us help you find a strategic, legally sound path to a debt-free life.