In the modern financial landscape, personal loans are often the go-to solution for immediate needs—be it a wedding, a home renovation, or an unplanned medical expense. However, life is unpredictable. A sudden job loss, a business downturn, or a family crisis can quickly turn a manageable monthly installment into a mountain of debt.

When you find yourself unable to keep up with repayments, the pressure from lenders can be overwhelming. This is where Personal Loan Settlement comes into play as a viable exit strategy. In this guide, we will walk you through the nuances of Loan Settlement India and how you can find Loan Relief without losing your peace of mind.

What is Personal Loan Settlement?

A personal loan settlement is an agreement between a borrower and a bank (or NBFC) where the lender agrees to accept a one-time payment that is significantly lower than the total outstanding amount. Once this payment is made, the lender considers the loan “settled” and ceases all recovery and legal actions.

It is important to note that banks typically offer this option only when a loan has been in default for more than 90 days (classified as a Non-Performing Asset or NPA) and they believe the borrower has no immediate capacity to pay the full amount.

The Step-by-Step Personal Loan Settlement Process

Navigating the Loan Settlement India landscape requires a strategic approach. Here is how you can manage the process effectively:

1. Evaluate Your Financial Capacity

Before approaching a bank, take a hard look at your finances. Determine the maximum lump-sum amount you can arrange. Since you are asking the bank to take a “haircut” (a loss on the interest and principal), you must have a clear justification for your financial hardship.

2. Initiation of Request

Contact your bank’s recovery or credit department. It is often beneficial to involve experts from a platform like Settle Loan at this stage. Professional mediators understand the internal language of banks and can help present your case of genuine hardship more convincingly than a stressed borrower might.

3. The Negotiation Phase

This is the heart of the Personal Loan Settlement process. The bank will initially ask for a high amount. Through negotiation, you aim to bring this down. Depending on the age of the debt and your specific circumstances, settlements can sometimes be reached at 25% to 50% of the total outstanding amount.

4. Obtaining the Sanction Letter

Once a verbal agreement is reached, do not make any payment yet. Demand a formal “Settlement Sanction Letter.” This document must be on the bank’s official letterhead and should clearly state the settled amount, the due date for payment, and the fact that the bank will drop all legal proceedings upon receipt of the funds.

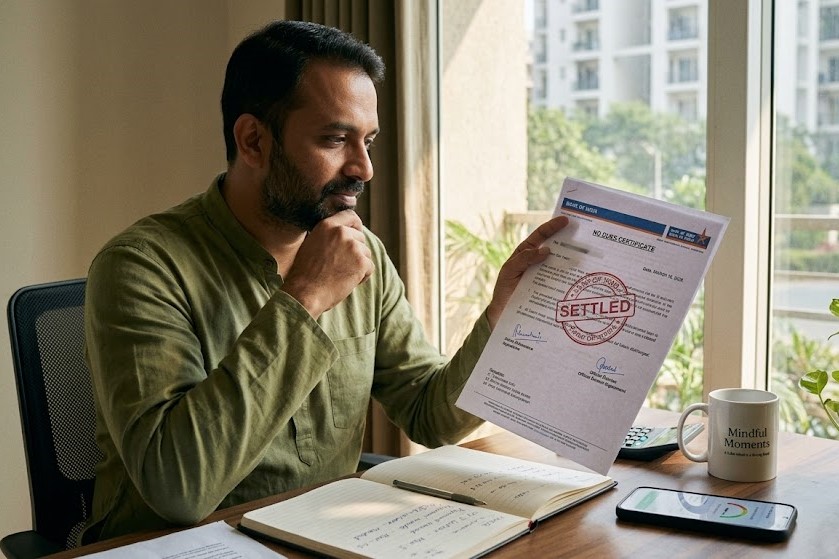

5. Final Payment and No Dues

Pay the agreed-upon amount within the deadline. After the payment is processed, ensure you receive a “No Dues Certificate” or a closure confirmation. This is your legal shield against any future claims regarding this specific loan.

Understanding the Impact on Your Credit Score

While Loan Relief provides immediate mental and financial freedom, it does come with a caveat. The loan will be reported to credit bureaus (like CIBIL) as “Settled” rather than “Closed.”

-

Settled: Means you paid less than what you owed. This can lower your credit score and make it difficult to get new loans for the next 2–3 years.

-

Closed: Means you paid the full amount. This is the ideal status for a high credit score.

However, if you are already struggling with defaults, a “Settled” status is often better than an “Active Default” status, as it allows you to eventually start rebuilding your financial profile from scratch.

Why Seek Professional Help?

The Personal Loan Settlement process can be intimidating. Banks often use aggressive recovery agents to pressure borrowers. By partnering with a specialized firm like Settle Loan, you gain a professional buffer. Experts handle the aggressive calls, manage the complex paperwork, and use their industry leverage to get you the lowest possible settlement figure.

Conclusion

Debt is a hurdle, not a dead end. By understanding the rules of Loan Settlement India, you can take proactive steps to resolve your liabilities and start fresh. You deserve a life free from the shadow of debt collectors.

If you are ready to take the first step toward financial freedom, visit https://settleloan.in for expert assistance and personalized Loan Relief strategies.