When financial hardship makes it impossible to continue paying your Personal Loan EMIs, you are typically presented with two primary resolution paths: loan restructuring or loan settlement.

Restructuring is always preferable as it preserves your credit score. However, there are specific, dire circumstances where choosing Personal Loan Settlement becomes the necessary, strategic, and most prudent option.

Here is a guide to help you understand when to make the critical switch from attempting restructuring to pursuing a Settle Loan agreement.

1. Understanding the Alternatives

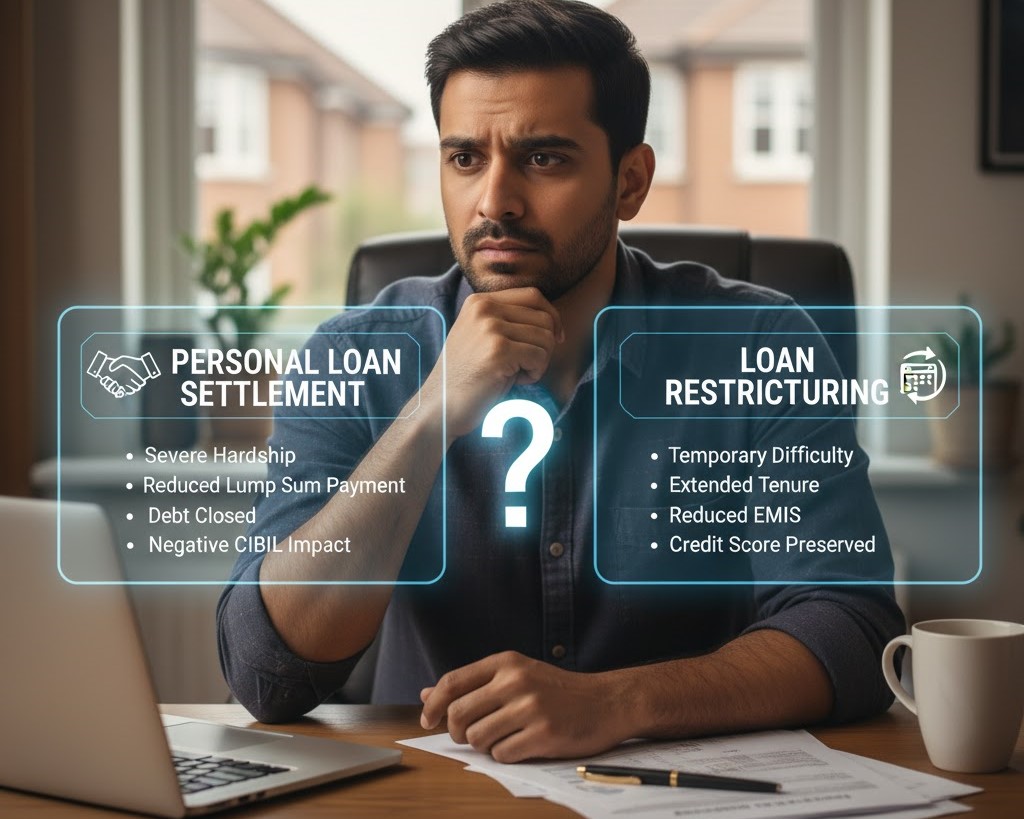

Before making a choice, it’s essential to know the fundamental difference between the two options:

| Feature | Loan Restructuring | Personal Loan Settlement (OTS) |

| What It Is | Temporarily changing the loan terms (e.g., extending tenure, reducing EMI, offering a moratorium). | Paying a reduced, lump-sum amount to close the entire debt. |

| Credit Score Impact | Minimal Negativity. The account remains “current” or is marked as “Restructured,” which is a small hit. | Severe Negativity. The account is marked “Settled,” severely dropping your score for up to 7 years. |

| Cost | You pay the full principal and interest (sometimes more due to extended tenure). | You save a large portion of the principal and accrued interest/penalties. |

| Goal | To continue repayment and avoid default. | To close the debt entirely and move on. |

2. When Settlement Becomes the Strategic Choice

While restructuring avoids the catastrophic credit hit, Personal Loan Settlement (OTS) is the necessary choice under these specific conditions:

A. When Financial Hardship is Permanent or Extreme

- Permanent Loss of Income: If you or the primary borrower has faced a permanent, severe loss of income (e.g., irreversible disability, long-term unemployment with slim prospects, or business failure).

- Insolvency: If your current liabilities (total debt) significantly outweigh your current and foreseeable future assets and income. Settlement offers legal finality when bankruptcy is the only alternative.

B. When Restructuring Offers No Real Relief

- Unmanageable EMI: The bank’s restructuring offer (e.g., extending the tenure by two years) still leaves you with an EMI that you know you cannot consistently afford, leading to the near certainty of a future default.

- High Interest: Your Personal Loan has such a high interest rate that restructuring only adds years of compounding interest, making the final repayment amount enormous and not financially sustainable.

C. When You Have Access to a Lump Sum

- Available Funds: You, or a family member, can arrange a single lump sum of cash now (perhaps from an insurance payout, asset sale, or family help) but cannot commit to regular, long-term EMI payments. The promise of immediate cash is the bank’s biggest incentive to offer a settlement.

D. When You Value Debt Freedom Over Credit Score

- Priority Shift: You determine that being completely debt-free and closing a severe liability is worth the inevitable 7-year cost to your credit score. This is a common choice for individuals nearing retirement or those who do not anticipate needing major loans (home, car) for the next seven years.

3. The Settle Loan Finality

When you choose Personal Loan Settlement, you gain closure. You eliminate the liability entirely.

To ensure this finality, you must secure the Settlement Letter before paying anything, guaranteeing that the debt is closed in “Full and Final Settlement.” This action formally terminates the original loan agreement and allows you to budget for your life without the shadow of that high-interest debt.

Are your finances too strained for restructuring? Don’t risk a double default.